Login

Login On behalf of Scan Global Logistics

Global COO & CCO

Market update

08 Jan, 2024

During the weekend, isolated incidents were registered amongst others involving the US destroyer USS Laboon shooting down a drone in self-defence as the drone came within close vicinity of commercial vessels. Additionally, the UKMTO (UK Maritime Trade Operations) reported that six smaller boats approached a merchant vessel within one nautical mile, albeit no visible signs of attacks were evident.

Operation Prosperity Guardian not kicking into gear as expected

There are growing concerns about Operation Prosperity Guardian, the US-led coalition formed to ensure order is restored in the Red Sea, allowing vessels and seafarers to pass safely. While the Pentagon has announced that more than 20 countries have joined the coalition, concrete commitment and progress is still modest by nature.

While the US remains confident over the operation, only two handfuls of countries confirmed their active participation in the coalition, including the UK, Australia, Denmark, Norway, Bahrain, Canada, Greece, and the Netherlands.

Source:The Cradle

More notably, countries such as Spain, Italy, and France have not confirmed participation in the coalition, however, they have deployed naval ships to the area to serve their national interests and consequently distanced themselves from the US coalition umbrella. It is also worth noting that Bahrain is the only Gulf state taking part in the efforts to restore peace and order in the Red Sea. Egypt and Saudi Arabia are notable absentees despite a heavy reliance on trade in the region, with Egypt having, on paper, a fundamental interest in returning to ‘normal’ on account of the Suez Canal being under Egyptian ownership.

Some have compared the current situation with the pirate attacks near the coastline of Somalia some years ago; however, there are major differences. The operations in Somalia were backed by a clear UN mandate, with all permanent members of the UN Security Council supporting the operation. This is not the case for the current operation, which is solely led by the US coalition independent from the UN.

This ties to the nature of the attacks that have come in response to Israel’s operation in Gaza. The US has maintained strong support for Israel, while many other countries have maintained a more neutral stance in the conflict. Accordingly, these countries fear that participation in the US-led operation can be perceived as taking the side of Israel. This is the case for many Middle Eastern, African countries and as well some European countries.

It is overall premature to judge the success of Operation Prosperity Guardian. As highlighted, it has led to the prevention of attacks, but whether it is enough for the major container carriers to resume Suez Canal passage is unknown at the time of writing, and there are no concrete signs of this happening.

Hitting the news just a few hours ago, there is ongoing speculation that some carriers have entered into direct bilateral negotiations with the Houthi rebels in Yemen to strike a deal guaranteeing safe passage through the Red Sea. The demand in return from the Houthi is that shipping lines must accept and guarantee that they will not carry any Israeli cargo or dock in Israeli ports.

This news comes just a few hours after Cosco announced that it would no longer send ships to Israel through the Red Sea, fuelling speculation that Cosco is one of the carriers to have struck such an agreement.

According to Shippingwatch.com sources in the Middle East with in-depth knowledge of the process claim that other carriers have entertained same dialogue, albeit not naming these. Shippingwatch has reached out to Maersk, CMA CGM and Cosco for comments, but at present neither had offered any comments in response.[1]

With this news surfacing in recent hours, it is difficult to assess the full magnitude of this and whether European based carriers would be prepared to take such a step forward, indirectly taking a political stance in the conflict.

Supply & Demand unfold in full force

While the background for the current situation is tragic, much of the focus has been on the operational and financial impact on global trade. Ocean freight rates have been surging in recent weeks, reminiscent of the development during the COVID-19 pandemic, where rate levels skyrocketed, triggering historic profits for container carriers and, in return, much frustration on the shipper side.

So what is driving the development this time around?

The answer is simple - an instant and fundamental change in supply and demand, with available capacity rapidly decreasing.

During 2023, rate levels declined to near loss-giving levels for carriers on account of over-capacity, and thus, the supply and demand equation favoured shippers, providing much-needed relief from a cost perspective.

The debate has often centred around whether the industry will ever learn from these dramatic changes in rate levels, finding the magic key where both carriers and shippers can see eye to eye on what constitutes a win-win situation or at least avoid a lose-lose scenario.

The topic has become emotional, with shippers accusing carriers of profiteering on the back of a tragic situation and carriers conversely arguing that shippers have not been willing to pay sustainable rate levels for a decade.

The latest development, and in addition to this, the latest years of development during the pandemic, provides a straightforward answer: supply and demand rules, and it is a two-way street for better and for worse.

It is beyond discussion that most within the industry would wish for a less erratic rate development, as it is evidently stealing focus from more important topics such as sustainability initiatives and overall supply chain optimisation. At the end of the day, there is ultimately only one to pay - end consumers.

Container carriers need to plan and commit to billion-dollar investments basis highly uncertain economic crystal ball scenarios, leading to an almost constant irregularity between supply and demand. The most apparent learning from last year´s development is that it is impossible and practically illusionary to think that anything can be predicted with the only constant being change.

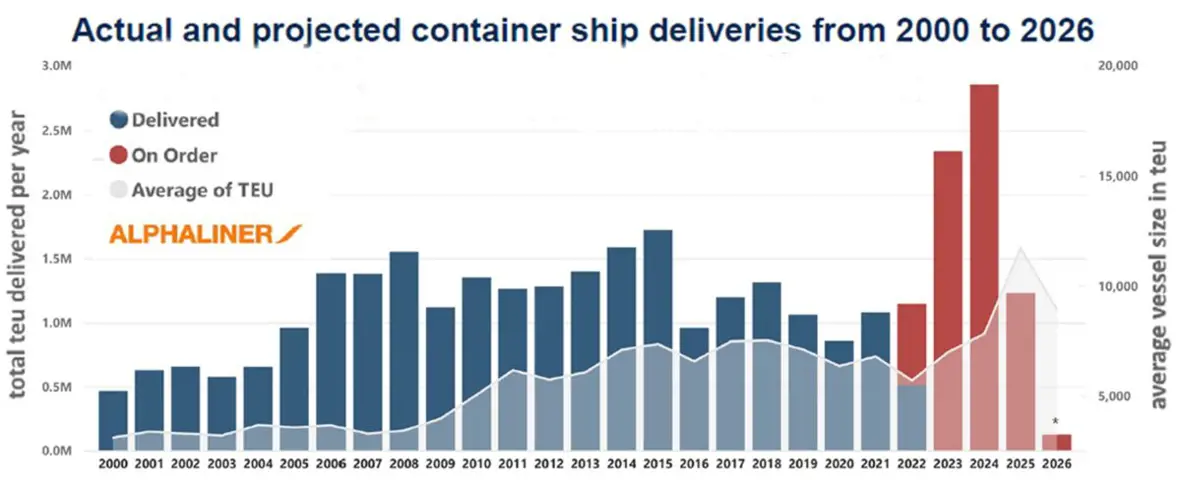

As can be seen in the below overview provided by Alphaliner, delivery of new vessels has, over the years, been quite irregular, with container carriers typically investing during upward economic cycles for the industry.

Source:The Zey Marine

In the “old” days, a simple theory called the GDP multiplier guided the expected demand for ocean freight capacity. For many years, the multiplier averaged around 1 to 3, i.e., growth in GDP of 3 %, as an example, would lead to an increase in ocean volumes of 9 %.

This is no longer the case, and the textbook needs to be rewritten, which presently has not been done in a manner that satisfies neither party in the industry. There are even those who occasionally state that the industry was healthier at the time of the conferences led by the FEFC (Far East Freight Conference), which, in essence, was a carrier cooperative where surcharges and rates were discussed under a legal framework.

The conferences ended in October 2008, effectively based on changes to the European Union's exemption of Shipping Conferences from their competitor regulations.

Supply & Demand 1-0-1

A quick online search provides the following definition of supply and demand:

“In microeconomics, supply and demand is an economic model of price determination in a market. It postulates that holding all else equal, in a competitive market, the unit price for a particular good or other traded item, such as labour or current financial assets, will vary until it settles at a point where the quantity demanded (at the current price) will equal the quantity supplied (at the current price), resulting in an economic equilibrium for price and quantity transacted. The concept of supply and demand forms the theoretical basis of modern economics”. [2]

As we speak, we are beginning to see the first signs of a capacity crunch, which, as a minimum, will be present up until the Lunar New Year in February. Ongoing dialogue with our carrier partners also points to an emerging shortage of especially 20´ equipment in Europe, and congestion at main ports is also expected, considering that normal schedules are out of sync.

It is also expected that cancellations of sailings in both ex-Asia and Europe will accelerate in the immediate future as part of new schedules settling in.

With all this in mind, the conclusion is there is no indication that supply and demand will not continue to rule the development of freight rate levels. Instead of arguing and debating this fact that has been evidenced over recent decades, we encourage proactive discussions on how to avoid a ‘one size fits all’ approach to pricing, ensuring that both short-term cost risk mitigation and long-term business goals are observed and factored in.

The hardcore capacity facts

As communicated previously, it is estimated that container carriers require approx. 4-6 additional vessels on top of the normal 12 vessels to cover schedules on a round-trip from Asia-Europe-Asia. This points to an approximate reduction in nominal net capacity of roughly 25-30 %, which is significant in any scenario. Yes, there has been over-capacity in the market, but not to the tune of 25-30 %, and here it is important to bear in mind that Q4 overall saw a normalisation of volumes vs. available capacity. Accordingly, rate levels were already on an upward trajectory when the current Red Sea crisis emerged.

Carriers are trying to close the gap by implementing so-called extra-loaders and taking vessels on short-term leases. In one example, highlighted by Lars Jensen, CEO Vespucci Maritime, Hapag Lloyd has taken the 3.400 TEU Zhong Gu Shan Dong on charter and deployed it on their MD2 service from Shanghai to Piraeus/Genoa and then returned to Ningbo and Shanghai. [3]

Typically, vessels of this modest size would not be deployed on an Asia-Europe sailing, evidencing that all tools in the toolbox are being utilised. As a side note, vessels of this size cannot sail at the same speed as larger vessels, and accordingly, the transit time is also extended here by up to two weeks, so irrespectively, volatility remains.

Rate levels surging, with plateau level in sight

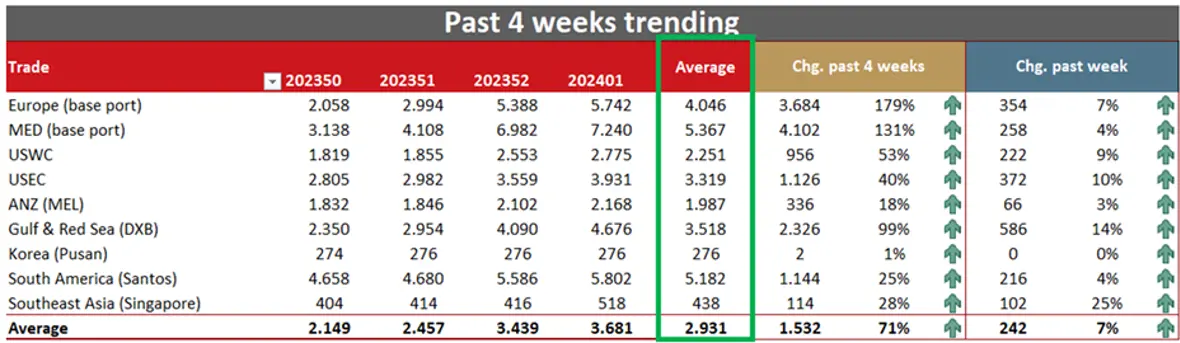

While week 52 resulted in an all-time high SCFI week-on-week increase with the rate level on the Far-East to Europe main port settling at + USD 5.300, up from USD 2990 in week 51, then week 1 offered a somewhat softer landing, removing the worst fears amongst shippers.

An increase of USD 354/40´ vs. the previous week was the result of Friday´s SCFI update on Europe Main Port, with a rate level now registered at USD 5.742/40´. Interestingly, all major global trades, without exception, including The US and Latin America, all registered increases once again, cementing the interconnectivity of the global trade-lane ecosystem.

SCFI update week 1

Short and long-term rate differential

As also seen during the pandemic, it is apparent that the gap between long-term contracted rates and short-term FAK and spot rates is increasing. This, in turn, makes it very difficult to discuss what the ‘market level’ is since we essentially are seeing two markets with very different rate levels.

One confusing element is the ever-present influx of different surcharges posted by carriers, i.e. War Risk, Peak Season or Operational Recovery Surcharge, just to name a few. At the end of the day, it is the total rate inclusive of all relevant surcharges that is relevant to benchmark.

The significant, short and long-term rate differential means shippers increasingly face a reality where xx % of their volume is shipped on long-term rates within the committed allocation, subject to some of the before-mentioned surcharges. In contrast, any volume on top of committed and approved allocation is subject to short-term spot rates, which are evidently much higher presently, as can be seen in the above SCFI overview.

We assess that rates for now have plateaued, and while minor increases in coming weeks are still expected, then we do not expect a return to the historic high levels seen during the days of the COVID pandemic.

We will increasingly guide our communication based on all-in rates and less so specific surcharges with different nomenclature, as we acknowledge this has the potential of causing confusion. Carriers have adopted very different approaches to this topic, however, at any time, we aim to make the world a little less complicated and this step to service this direction.

The forgotten Panama Canal challenges

In the midst of the prolonged crisis in the Red Sea and with the Suez Canal considered the most vital lifeline for global trade, the Panama Canal challenges have faded into the background despite this situation potentially having a more profound long-term impact exceeding the short-term issues in the Red Sea.

A friend of SGL shared an article with us published on 22 December 2023 in The Guardian headlined “Changing climate casts a shadow over the future of the Panama-canal and global trade”, serving as a healthy reminder that the industry is engulfed in a two-flank fight.

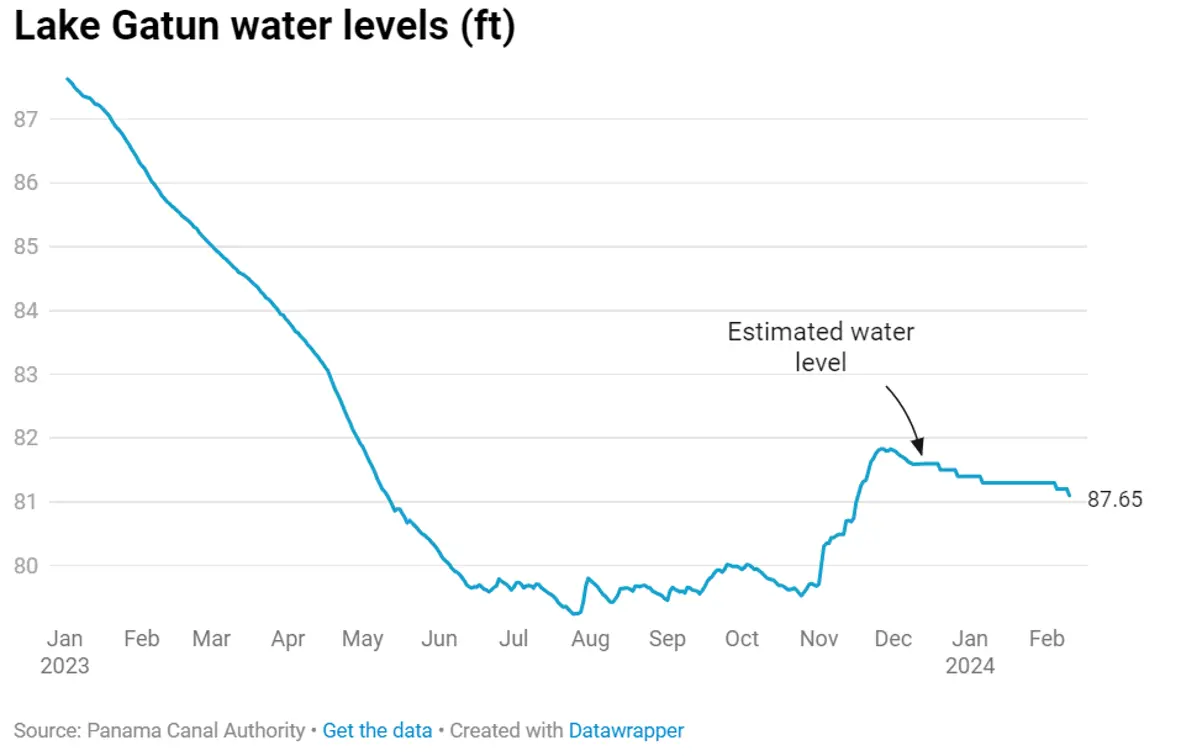

Vessels continue to idle at the Panama Canal due to low water levels caused by a historic rain deficit, which has prompted authorities to restrict the number of vessels passing through the canal.

Source: The Guardian

To put the issue(s) into perspective, in concrete terms, the water level is approximately 1.8 meters below the normal water level. According to reports, this has triggered an almost “bidding war” like situation with carriers desperate to get ahead of the queue.

According to the Guardian, more than 14.000 vessels traversed the Panama Canal in 2022, with more than 40 % of the goods traded between North and East Asia and the US East Coast transported through the canal.

Panama is one of the most rain-prone countries in the world, and accordingly, a significant drop in water level has never been an issue previously, with the surrounding lakes of the Panama Canal blessing the canal with an abundance of water. However, accelerated by the El Niño weather phenomenon, the water level in Lake Gatun has dropped to close to the lowest level ever recorded.

Under normal circumstances, the Panama Canal can handle 36 vessels daily but recently has had to reduce this to 22 vessels per day. It is expected to be further reduced to 16 per day in February. In other words, the math does not add up anymore, and the situation is growing increasingly critical.

As outlined by the Guardian, carriers, in essence, are faced with three options: wait up to several weeks to pass, pay up to USD 4 million per passing to jump ahead in the queue or find alternative routings, adding days and weeks to the originally scheduled transit time. As highlighted on a few occasions, the Suez Canal routing has, in recent months, increasingly been used for Asia-US East Coast cargo as well, with global shipping challenges coming full circle.

In more precise numbers, the Panama Canal handles approx. 3-4 % of global maritime trade and up to 45 % from Asia to US-East Coast. While 3-4 % might not sound critical in itself, it is, in reality, a significant number considering the vulnerability of global shipping, as evidenced in recent years.

It was further outlined that the risks do not merely come in the form of financial impact and delayed cargo but also an increased security risk, with vessels finding it increasingly difficult to find suitable anchorage spots, risking collisions with other anchoring vessels.

On a further dark cloud note, projections currently show that March and April could spell even lower water levels in Lake Gatun. Accordingly, there is no outlook for an improved situation at the Panama Canal, with the challenges being nature-driven as opposed to human intervention in the Red Sea.

Source: The Guardian

A one-off situation or a new normal?

Panama Canal authorities have commented that it is: “implementing operational and planning procedures, innovative technologies, and long-term investments to mitigate the impact and safeguard the canal’s operation” and continue “, it could not have predicted exactly when the water shortage would occur to the degree that we are experiencing now”, however, critics say that climate change has been a present threat for a long time and measures should have been taken earlier to protect global trade.

According to experts, the long-term answer to the sustained water level shortage will be to dam up the Indio River and then drill a tunnel through a mountain to pipe fresh water 8 kilometres (5 miles) into Lake Gatun, a project estimated to cost + USD 2 billion.

While this solution sounds straightforward and, under the circumstances, a cheap investment, moving the proposal forward is challenging, considering it impacts thousands of local farmers and ranchers whose lands would be flooded for the reservoir to be filled.

What to expect in coming weeks?

As informed, we short-term do not expect carriers to resume Suez Canal passage and accordingly pro-longed transit times are to be factored in when planning orders. Additionally, until further notice and minimum through Q1 and into Q2, we project rate levels remain elevated as a direct consequence of reduced capacity, and this projection is factoring in the Lunar New Year period in February.

Further ripple effects are also expected in the coming weeks in the form of equipment shortages both in Europe and Asia. Furthermore, we expect an increasing number of sailings to be cancelled despite carriers implementing extra loaders to mitigate the worst consequences.

On the airfreight side, we have multiple solutions for urgent shipments, including Sea-Air options. We encourage proactive dialogue with our teams on these solutions, which is also the case for rail freight to and from Asia-Europe.

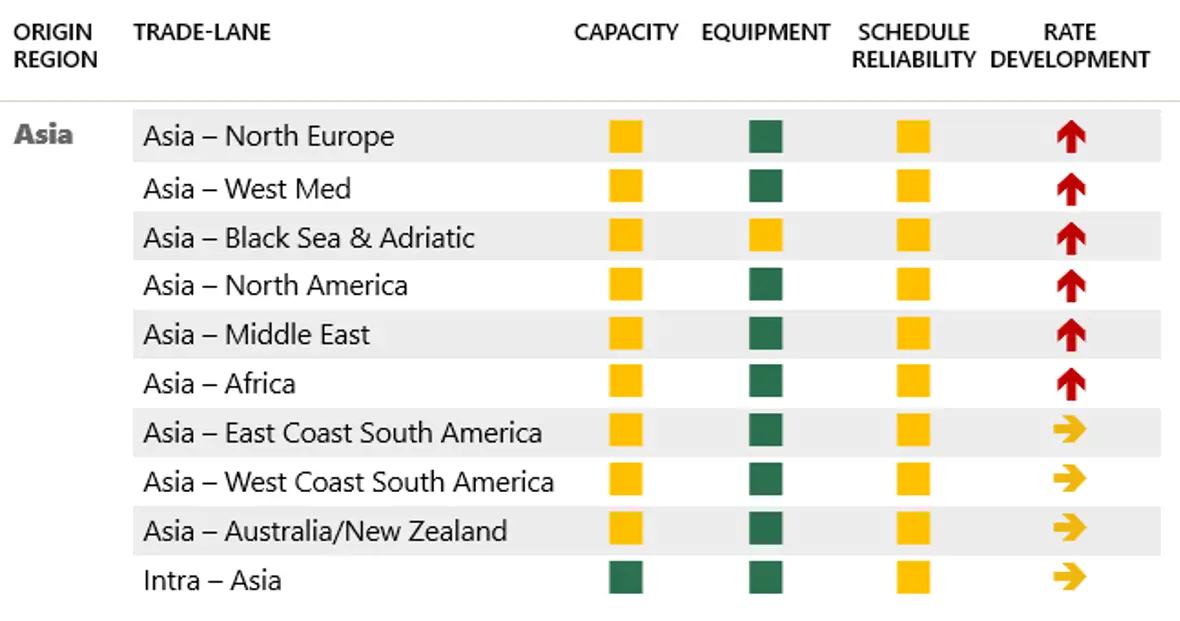

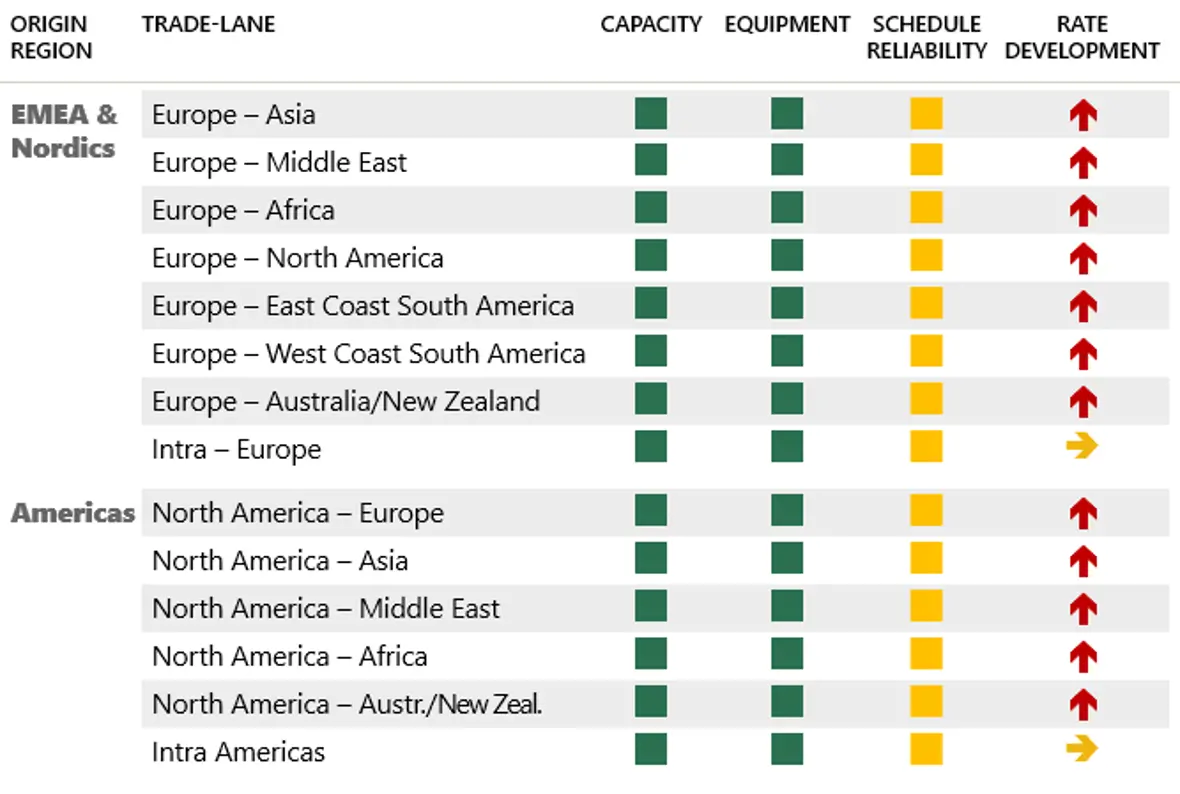

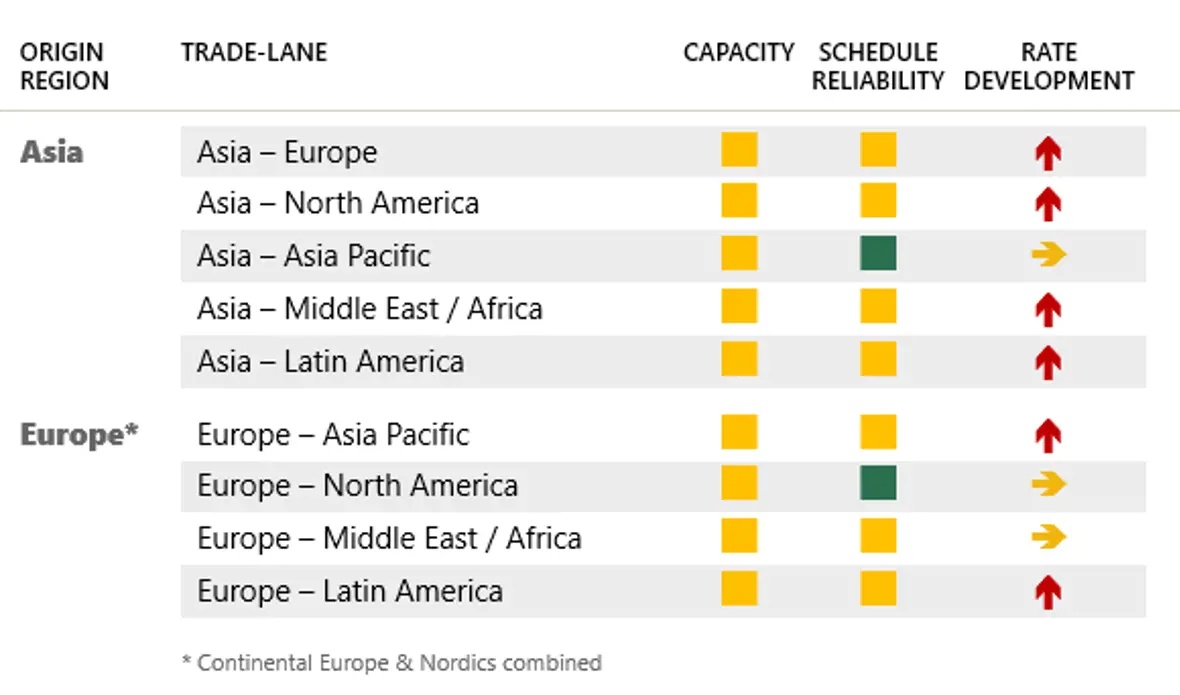

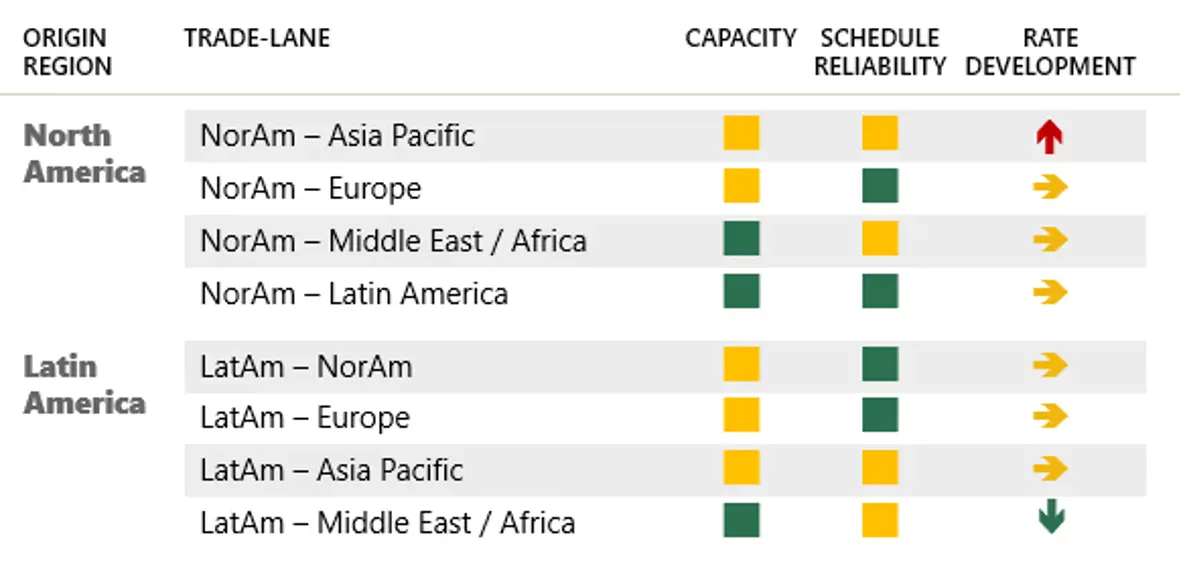

For an overall status on air, ocean, and rail freight, please see below:

OCEAN FREIGHT

AIRFREIGHT

RAIL FREIGHT

Our teams are working around the clock to keep you duly informed both in terms of potential delays and, not least, in terms of alternative solutions.

All the above information is given to the best of our knowledge and is subject to change.

[1] https://shippingwatch.com/carriers/article16738006.ece

[2] https://en.wikipedia.org/wiki/Supply_and_demandhttps://shippingwatch.com/carriers/article16738006.ece

[3] https://www.linkedin.com/posts/larsjensenvespuccimaritime_day-23-of-the-red-sea-crisis-us-destroyer-activity-7149642021308207104-C0xI?utm_source=share&utm_medium=member_desktop

On behalf of Scan Global Logistics

Global COO & CCO