Login

Login On behalf of Scan Global Logistics

Global COO & CCO

Market update

23 Jan, 2024

Both Houthi rebels and the US have launched new attacks in recent weeks, and as we speak, there is no sign that the conflict is de-escalating. Despite attacks on strategic Houthi infrastructure, it is clear that the coalition led by the U.S. is showing restraint, and the attacks do not constitute a full-scale attack. According to analysts, this approach is a clear indication that there is a high degree of sensitivity attached to the U.S. and other allied coalition countries engaging in pro-active military attacks in the Middle East owing to the rich history of instability in the region.

Similarly, the Iran-backed Houthi rebels are not backing down, as seen with numerous attacks during the latest days, thankfully still without any casualties amongst crew members.

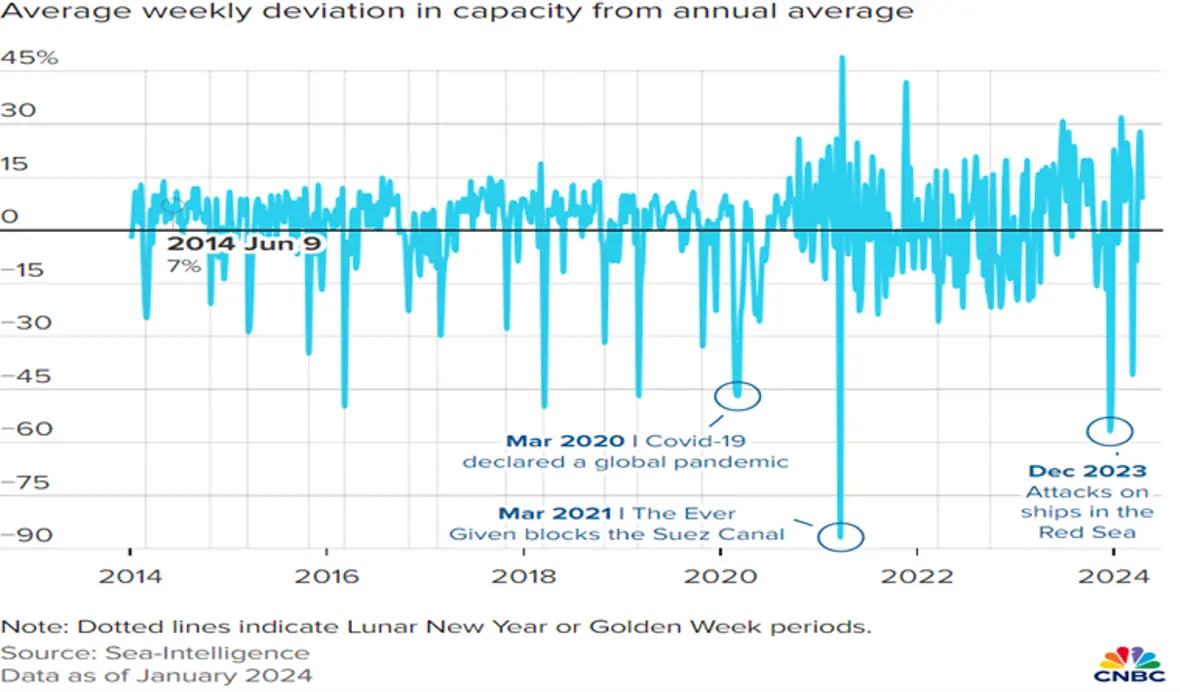

Red Sea attacks already bigger issue for supply chains than the pandemic, maritime advisory warns

What many projected to be a short-lived crisis during the early days is edging ever closer to a situation reminiscent of the challenges that wreaked havoc on global supply chains during the COVID-19 pandemic.

An article published by CNBC on 18 January displayed a headline emphasising this specific point: ‘Red Sea attacks already bigger issue for supply chain than pandemic, maritime advisory warns’.

The article zoomed in on the ripple effects caused by the necessity of re-routing the Cape of Good Hope, including a detailed analysis done by Sea-Intelligence on vessel delays compared to delays during recent years, ultimately concluding that the impact in isolation is greater than what was seen during the pandemic.

Allan Murphy, CEO of Sea-Intelligence, outlined it clearly: ‘The vessel capacity drop is the second largest in recent years’ and continued ‘The only single event with a bigger impact than the Red Sea crisis was the ‘Ever Given,’ the giant cargo ship which got stuck in the Suez Canal for six days during March 2021. Billions in trade were at a standstill during that event. With that exception, this [the Red Sea crisis] is the largest single event – even larger than the early pandemic impact’.

With this said, there is one significant difference between now and the pandemic days: the actual demand is lower. Demand during the pandemic was fuelled by an unprecedented spending spree by global consumers, which is not the case this time. Moreover, ocean carriers have injected significant capacity during 2023, softening the current blow.

The current delays and projected longer transit times are already impacting companies across the globe. Companies such as Tesla, Volvo and Michelin have communicated that they have been forced to halt production due to shipment delays. Similarly, IKEA and other global retailers have warned of product delays during the coming months.

Steve Lamar, CEO of the American Apparel and Footwear Association warned: ‘delays and cost increases are mounting. Although companies are exploring alternative shipping options, adverse knock-on effects continuing to disrupt logistics globally. More needs to be done to ensure the safety of crews and security of cargo by eliminating existing or future threats entirely’.[1]

This marks another reminder that the current challenges have ‘gone global’ with US shippers equally impacted by the current situation, as evidenced by surging ocean freight rates.

Attacks in the Red Sea intensifying

Despite US-led efforts to restore peace in the area, the coalition attacks on Houthi rebels have so far had an adverse effect, with Houthi attacks intensifying as a response. On 18 January, the Chem Ranger, a chemical tanker, was attacked with two missiles launched at the tanker, however, not hitting its target. This follows a drone attack on the Genco Picardy vessel attacked earlier in the week, with the Indian navy releasing pictures of the damages.

Source:The Maritime Executive

There is continued concern from analysts on the weakness of the coalition due to the lack of regional support. The regional powerhouses such as Saudi Arabia, the UAE and Egypt remain notable absentees from the coalition.

While a considerable number of attacks have been repelled, the recent attacks do show that Houthi rebels can strike against commercial vessels, ultimately squashing any hope from the larger container carriers that a return to the Suez Canal is imminent.

The birth of the Gemini alliance courtesy of Maersk and Hapag Lloyd

Last week, the breaking news headlines were out in full force, with Maersk and Hapag Lloyd announcing the formation of the Gemini alliance, effective February 2025.

While some form of alliance re-shuffling was expected, the news was unexpected considering Maersk, in Q1 2023, following the announcement of the 2M divorce with MSC, communicated that being a member of a vessel sharing alliance (VSA) was ‘not compatible with its global integrator aspirations’.[2]

Confirming widespread speculation amongst analysts that Maersk simply does not have enough vessels to operate independently, Maersk, with the launch of Gemini, now appear to have made a different assessment of the current market situation.

During the presentation of Q4 2022 results a little less than a year ago, Maersk CEO Vincent Clerc stated that he did not expect the end of 2M to induce a ‘role of musical chairs that has been talked about, with everybody trying to find a new partner’.[3]

The launch of Gemini, marking a complete U-Turn in terms of what was previously communicated, was accompanied by a statement by Vincent Clerc stating, ‘We are pleased to enter into this cooperation with Hapag-Lloyd, which is the ideal sea freight partner for our strategic journey’.

Hapag Lloyd CEO Rolf-Habben Jansen was equally jubilant: ‘Teaming up with Maersk will give a boost to the quality we deliver to our customers,’ said Rolf Habben Jansen in the announcement.

Source: Maersk and Hapag-Lloyd Embark on a Sea Change with "Gemini Cooperation" - BBN | Breakbulk.News™"

It is important to note that the new Gemini cooperation is operational cooperation only. Vessel Sharing Agreements (VSAs) have been a standard in the industry for decades and will likely continue to be so for many more years.

Hapag Lloyd CEO Rolf Habben Jansen also took the opportunity to clearly state that ‘This does not represent a change of strategic direction for Hapag-Lloyd. We remain fully focused on liner shipping and the closely connected terminal and inland operations. We have no intention to become a logistics integrator’.[4]

The Facts & Numbers behind the new Gemini alliance:

With the above numbers mentioned, it is important to note that trades such as Oceania, Intra-Europe, Intra-Asia, Africa, Europe-Canada, India-North America, Latin America to Asia and Europe are not a part of the new alliance.

Maersk and Hapag direct port calls to decrease at the expense of shuttle-feeders

In a somewhat fundamental change aimed at increasing on-time reliability with a Gemini target of 90 %, Maersk and Hapag will increasingly rely on feeders (introduced as shuttles in the joint announcement) to connect port pairs. In essence, this means some ports called directly today by main vessels will, going forward, be serviced by feeder services.

The strategy behind this shift away from less direct port calls is rooted in the ambition of increasing reliability and shortening transit times. Simply put, by having main vessels call fewer ports, the expectation is that there is less risk of delays and less time spent idling in ports.

As one example, Maersk has serviced the port of Aarhus, Denmark, as a direct main vessel call from Asia's main ports. However, the first indications from published Gemini network plans indicate that this will no longer be the case. Instead, Maersk will utilise feeder services to cater for shipments to and from Denmark.

It remains to be seen how customers will greet this shift and whether other carriers and alliances will follow this trend. In recent years, the stability and certainty offered by direct overseas port calls have been heralded, given that this solution entails no risk of missed connections during transhipment.

Hapag Lloyd leaving THE Alliance partners alone on the dancefloor

As a natural consequence of the new alliance, Hapag Lloyd has officially issued a notice to leave its current alliance, THE Alliance, which, in addition to Hapag Lloyd, consists of ONE, Yang Ming and HMM.

With Hapag having been the largest capacity contributor in THE Alliance, it is widely considered that some form of further alliance re-shuffling is in the cards. It is considered unlikely that the remaining THE Alliance members can continue the alliance without Hapag. Accordingly, the coming months will be filled with speculation on who joins whom on the alliance dance floor.

Speculation has already surfaced as to whether the third major ocean freight alliance, Ocean Alliance, will utilise this opportunity to bring on board one or more of the current THE Alliance members.

The spotlight naturally falls on MSC, the world's largest container carrier, and whether MSC will seek to replace Maersk as partner or, indeed, remain independent from major alliances as the only global container carrier. It is considered that MSC is, in fact, the only container carrier that has a fleet enabling this; however, with 2M officially only ceasing at the end of 2024, this would be premature to confirm.

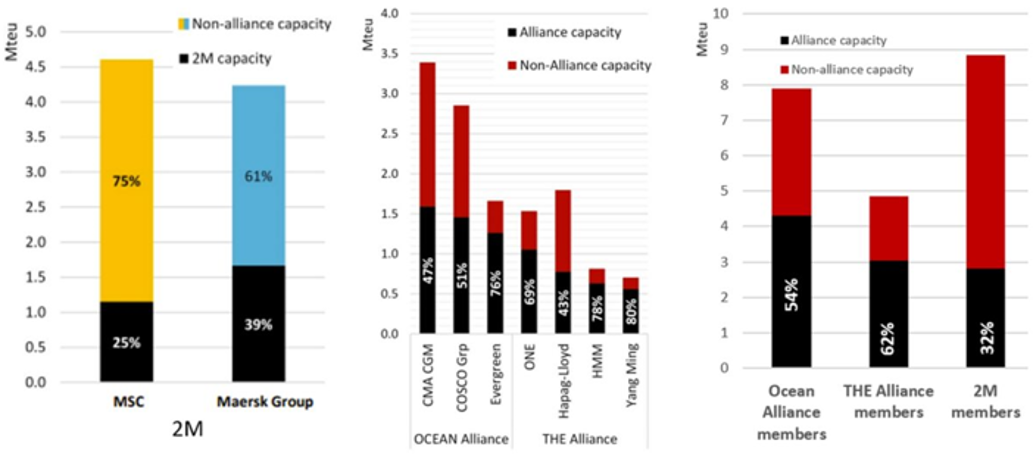

Below overview provided by Freightwaves in February 2023 illustrates the total capacity across the current alliances, divided into alliance and non-alliance capacity.

Across the current three major ocean freight alliances, there is a total of nine container carriers controlling approximately 83 % of the total global capacity. However, contrary to the general perception, these nine carriers only allocate 39 % of the combined total capacity to the three alliances.

Not surprisingly, the largest carriers allocate the lowest % of their total capacity to their respective alliances. Conversely, the smaller carriers contribute to the alliances with a significantly higher % share of their total capacity.

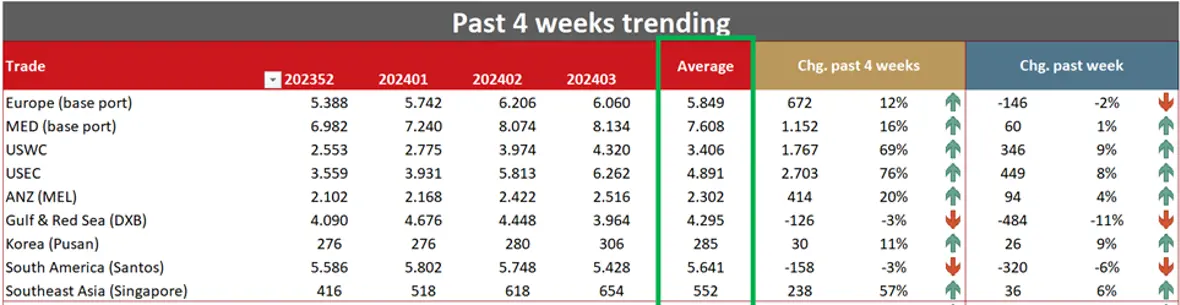

Ocean freight rates remain elevated amidst prolonged Red Sea challenges

In the latest SCFI (Shanghai Freight Index) update published on 17 January, the majority of trade lanes continued the upward trajectory; however, on Asia-Europe, the trend seen in recent weeks was halted with a modest decrease of USD 146 USD 6.206/40´ to USD 5.849/40.

There is a clear indication that rate levels are plateauing, removing the worst fears, that we yet again could see 5-digit rate levels as was the case during the COVID-19 pandemic. With this said current rate levels on Asia-Europe have doubled since week 51, where the base rate from Asia-Europe was listed at USD 2994/40.

On both the US West and East Coast, rate levels continue to increase, albeit at a slower pace.

On this side of the Lunar New Year, our prediction remains that rate levels will be sustained at current levels with modest upward and downward movements.

The current big joker remains whether we will experience significant container equipment challenges again. If this scenario materialises, this will likely sustain rate levels at current levels even after the Lunar New Year.

If this is not the case, we foresee some rate level normalisation throughout Q1, especially for Asia-Westbound and Trans-Pacific Eastbound.

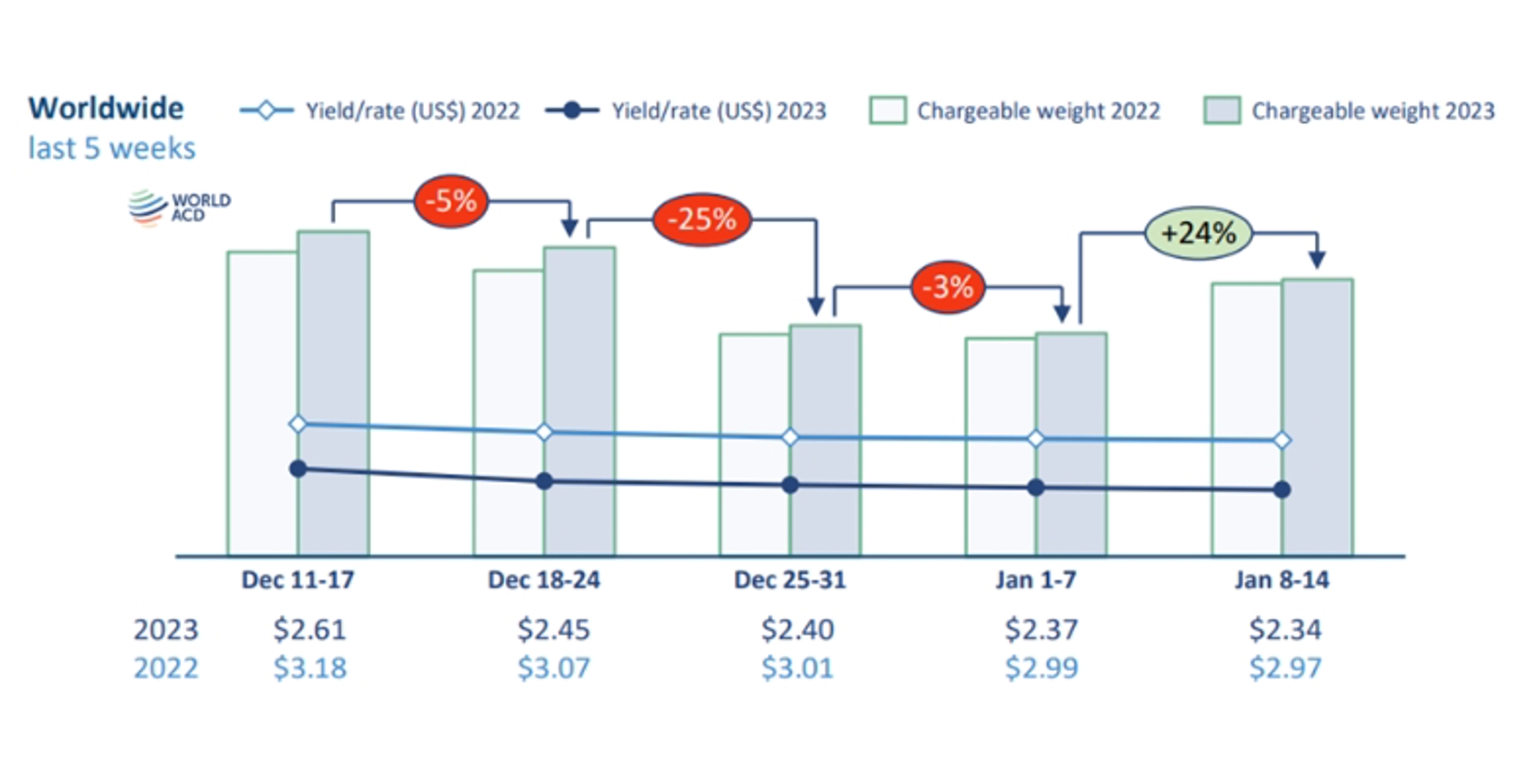

Airfreight enjoys ocean freight tailwind; however, no volume tsunami is in sight

An increase in airfreight, sea-air, and rail freight volumes is apparent, but not at a magnitude with the potential for significant disruption.

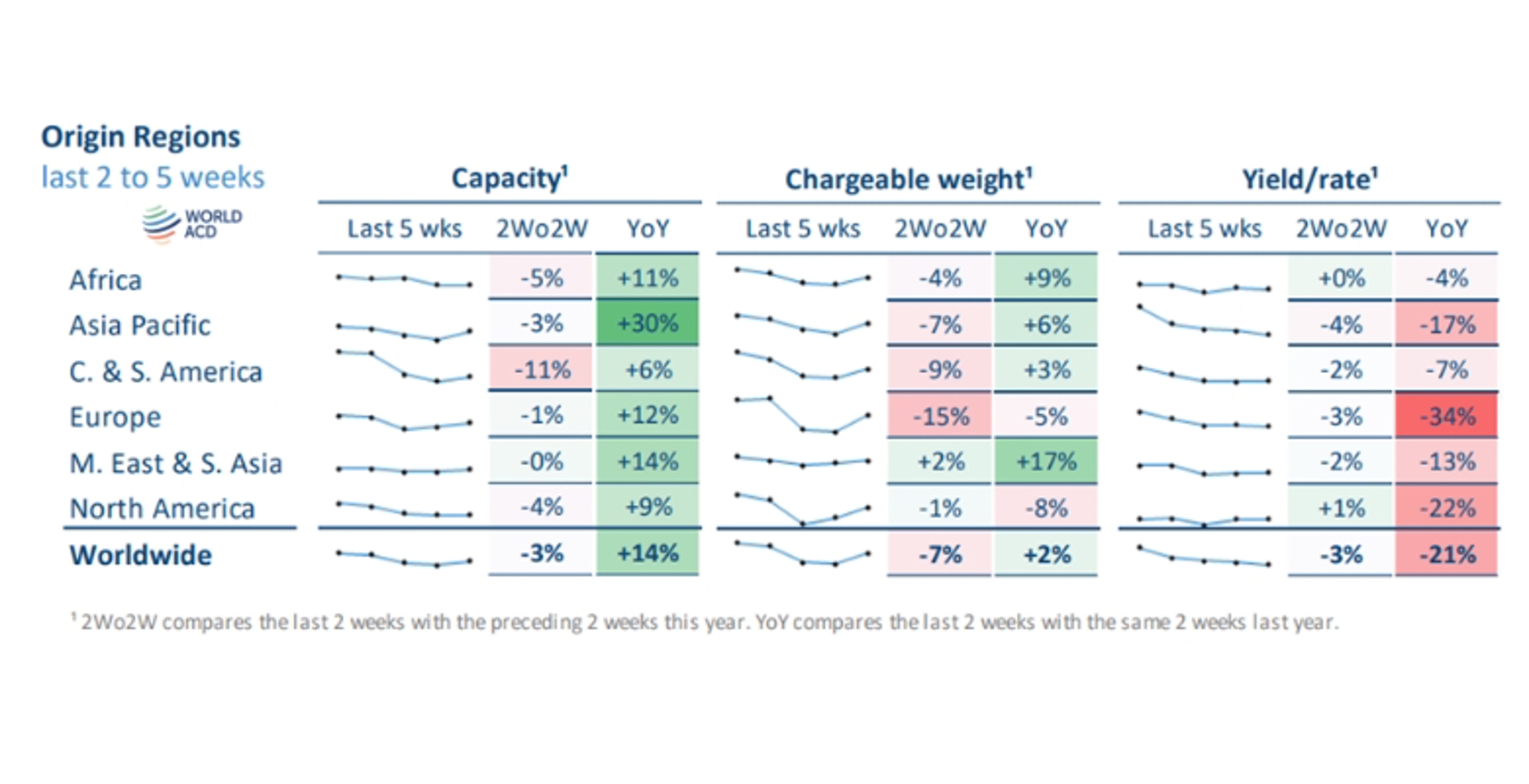

On the airfreight side, the development is clear, as seen in the below overview published by World ACD, with a noticeable week-on-week increase of 24 %.

This development is expected to be sustained until the Lunar New Year, and as a natural consequence, airfreight rates have also increased in recent weeks.

Source:WorldACD.com

Sea-air solutions remain popular, providing a ‘hybrid’ alternative, and we are on standby to support any urgent shipments.

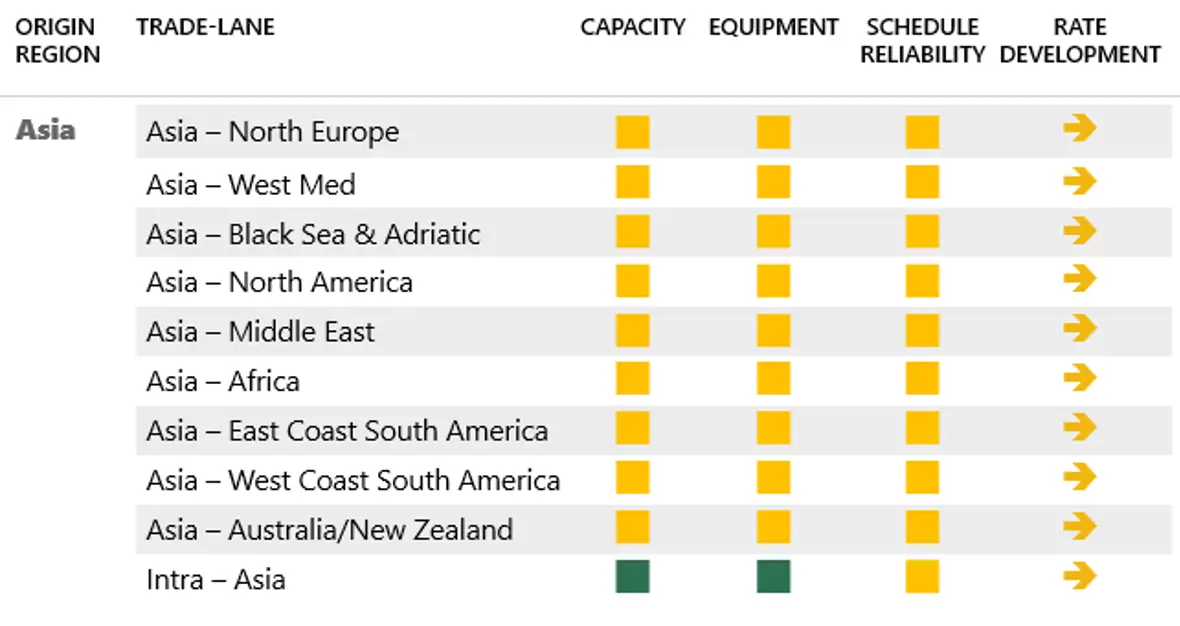

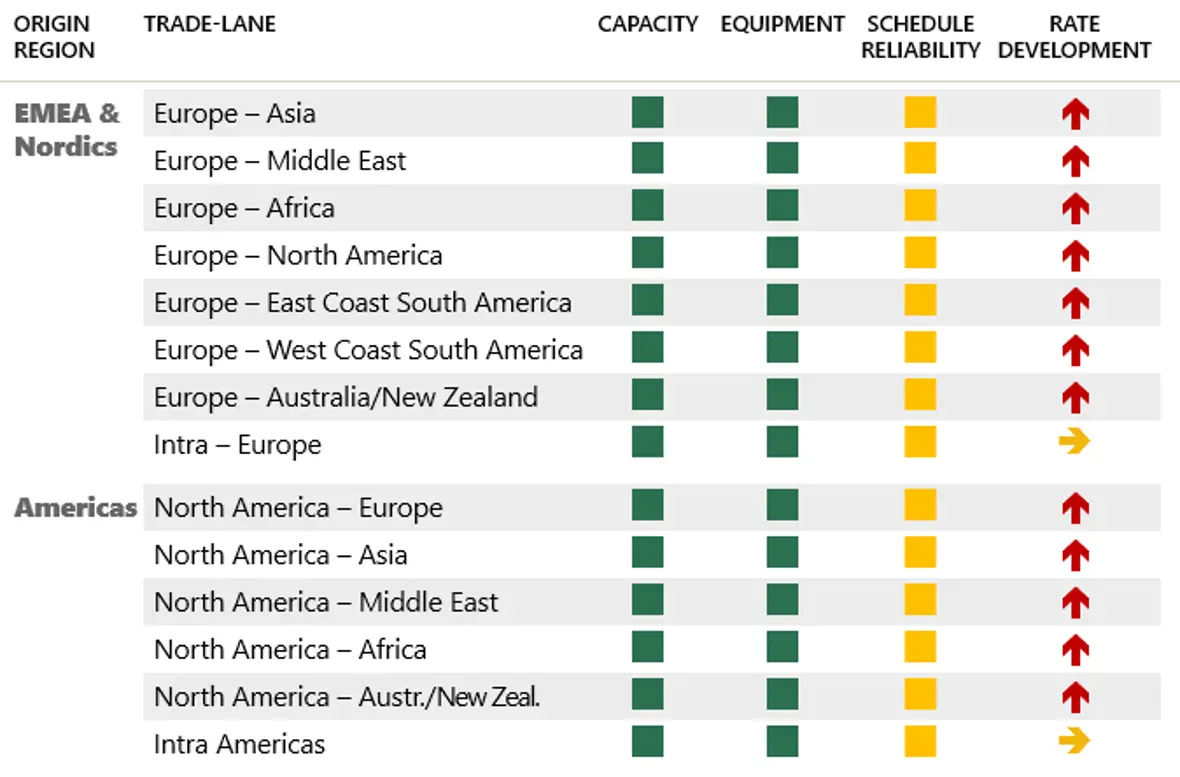

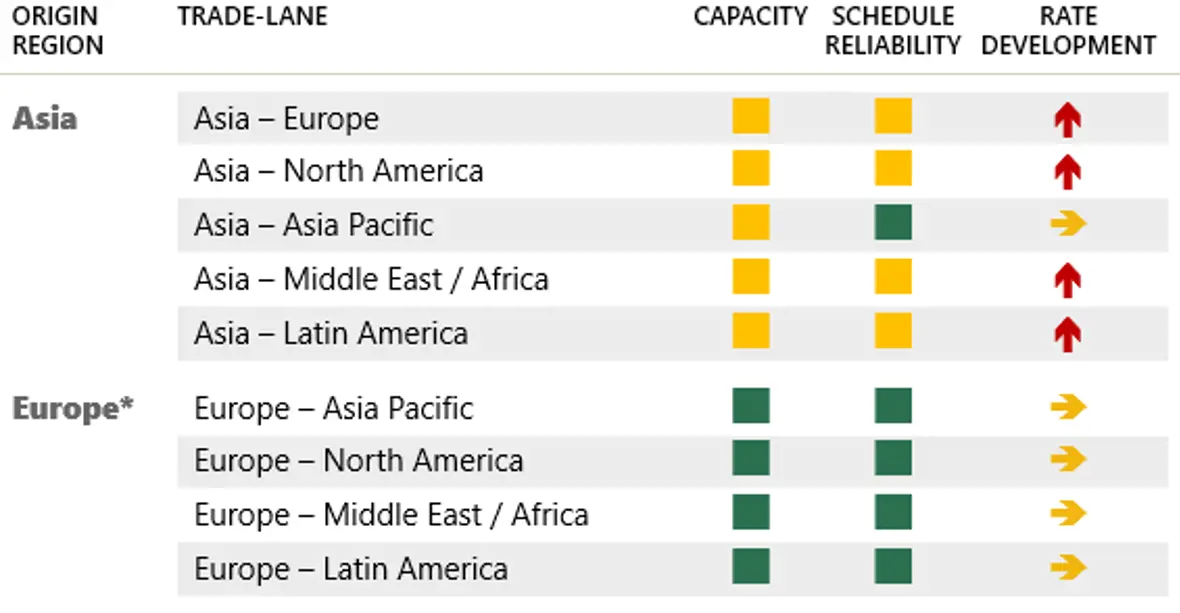

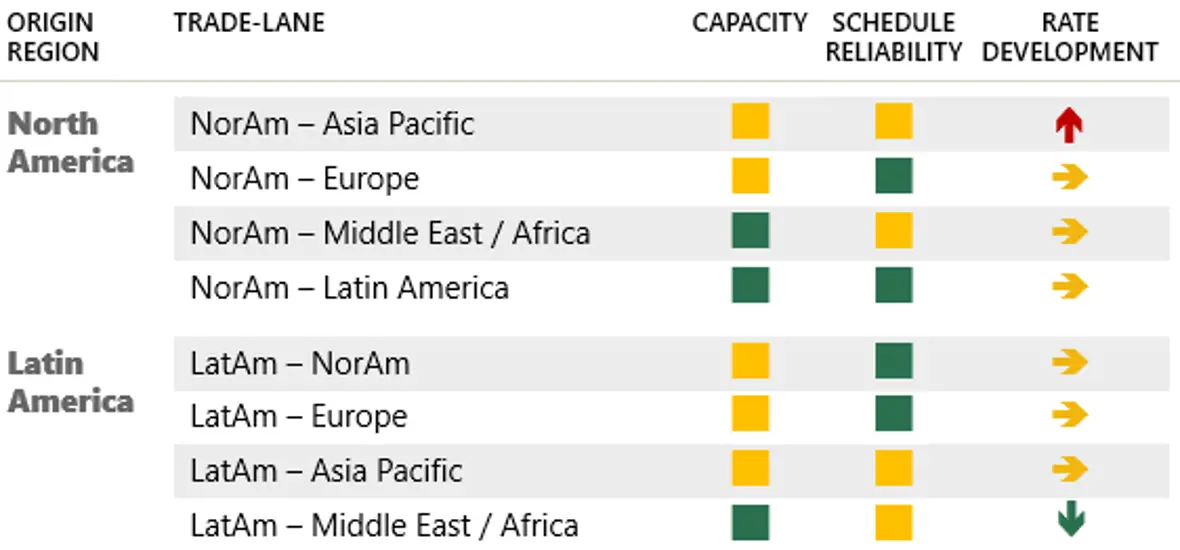

To get a complete overview of the trade lanes, please see below:

OCEAN FREIGHT

AIRFREIGHT

RAIL FREIGHT

As always, our teams are working around the clock to keep you duly informed both in terms of potential delays and, not least, in terms of alternative solutions.

All the above information is given to the best of our knowledge and is subject to change.

[1] Red Sea crisis already bigger issue for shipping than Covid, data show (cnbc.com)

[2] Maersk lays out integrator plan: no new alliance, post 2M - The Loadstar

[3] Maersk lays out integrator plan: no new alliance, post 2M - The Loadstar

[4] Maersk/Hapag Gemini Cooperation takes liner industry by surprise - The Loadstar

On behalf of Scan Global Logistics

Global COO & CCO