Market update

29 Jun, 2023

Irrespective of engaging in dialogue with experts on the supply or customer side, the consensus seems to be that the rest of 2023 will remain a 'wait and see game', and consequently, no major earthquakes in terms of rate development nor lack of capacity posing a challenge.

Yes, demand is slowly but surely picking up after a near meltdown in the power trades from Asia during Q1. However, we are, overall, not close to a scenario where demand will exceed supply.

Similarly, the 'over-stocking' syndrome is fading, with inventory levels decreasing significantly during recent months both in Europe and the US. This, coupled with consumers adjusting to a new reality, has triggered a volume rebound that especially carriers and airlines have desperately awaited.

With 2023 providing much needed relief in the form of normalized rate levels, improved reliability and an overall more stable marketplace, it's also time to ponder over what lies ahead.

Have all supply chain pain points from recent years magically been fixed overnight?

In our assessment, the answer is no. We have seen significantly less pressure on these supply chain pain points, such as congestion and lack of labour on account of the massive drop in volumes seen in 2023. However, at some point, volumes will rebound to pre-pandemic levels, and this could trigger a 2.0 supply chain crisis, albeit in a milder version than seen during the pandemic.

In other words, the current supply and demand situation is somewhat artificial by nature. Yes, we have been in a recession-like environment for some time. Still, GDP growth across Western economies has not been down by percentages that are even remotely close to the volume drop seen, and accordingly, the first half of 2023 should be seen as a correction phase.

What does the financial crystal ball have in store for us?

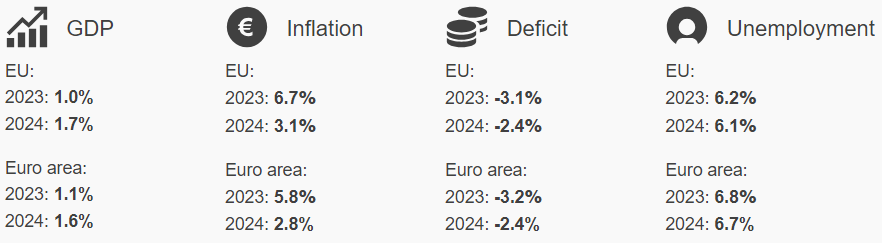

Although the latter part of 2022 and the first half of 2023 witnessed historically high inflation rates, soaring energy prices, and a general cost of living crisis due to the tragic war in Ukraine, the major economies have largely weathered the storm.

For example, the EU economy performed better than expected during the winter months. Many anticipated a recession in Q1 and continued economic contraction, but instead, we saw a modest 1% GDP growth. This growth occurred despite monetary institutions using all available tools to control inflation, which has been successful as inflation levels continue to decrease rapidly.

As we have seen in recent years, general economic development is closely tied to geo-political events which are ever present in the world we live in today. So, despite relatively healthy underlying economic indicators, why are consumers and companies still somewhat constrained in terms of spending and investments? The answer is geo-political uncertainty and volatility.

It is very difficult to open a news outlet without facing breaking news of some sort stemming from the geopolitical world.

The war in Ukraine rages on with no outlook of any form of peace, a dramatic increase in tension between the world's two superpowers, the USA and China, concerning Taiwan, and, latest as writing these words, political unrest within Russia itself.

The verdict is clear from consumers. They are adopting a 'wait and see' approach, leading to modest GDP growth rates in the foreseeable future.

Will geo-politics then impact global sourcing patterns?

Zooming in on the almighty superpower grudge match between USA and China, ocean carriers and airlines, like the rest of us, are uncertain about how the economic outlook will unfold. That leaves the question: Will the current and last years' events have any fundamental changes to global trade as we know it?

In the context of the current war in Ukraine, the Chinese government appears to be nourishing an image of impartiality as the country needs to retain good trading relations with both Russian and the countries opposing Russia. On the other hand, the US has embraced a more polarising approach, emphasising the concept of 'friend-shoring' or 'near-shoring' to diversify sourcing bases and ensure reliable supplies.

'Rather than being highly reliant on countries where countries have geopolitical tensions and can't count on ongoing, reliable supplies, the new doctrine is to diversify our sourcing base,' said Janet Yellen, US Treasury Secretary last year.

Friend-shoring, in essence, means that we have a group of countries that have a strong adherence to a set of norms and values ... and we need to deepen our ties with those partners and work together to make sure that we can supply our needs of critical materials,' she added.

So, is this materialising or not?

If we consider this in the context of a general deglobalisation in its many forms (either friend-shoring, near-shoring or re-shoring), then there is no data to support a fundamental shift to any significant degree. Still, clear indicators suggest a more diverse offshoring strategy, most notably known as the China+1 movement.

Drewry has conducted a study among its shipper clients to understand how current geopolitical instability influences their sourcing decisions.

While the study by no means is representative, the results do indicate that the notion of a general manufacturing relocation is overblown. Of the 66 respondents, only 15, or 23 %, said that their company has changed its main country of manufacture in the past five years. Other challenges ranked higher include trade disputes, rising labour costs, ethical concerns, and environmental considerations.

So, drawing a direct line between sourcing countries and the fear of logistics disruption does not seem correct. The thesis of deglobalisation seems more to have the form of an academic theory enabled by industry media hype.

With this dose of macro and geo-political information, it is time to deep-dive into the world of ocean and airfreight.

Please note that all information is given to the best of our knowledge and is subject to change.

Enjoy the onward reading!

On behalf of

Scan Global Logistics

![]()

Global COO & CCO

Airfreight market update week 26, 2023

It is no secret that this year promises to be difficult for container carriers. While carrier executives have been touting that demand growth will be reinvigorated in the second half of the year, that seems unlikely to offset the capacity surge. It has long been known that the sizeable volume of newbuild containerships due 2023 (and 2024) was going to force a market correction in the absence of any of the extra-ordinary port congestion and equipment shortages factors that had underpinned the extreme profits of the past few years.

As an early indicator that carriers are preparing for stronger measures, if markets continue to soften, they have started laying up more ships. Drewry research shows that the idle fleet increased by just over 300,000 teu in early March to reach a total capacity of 1.37 million teu. Drewry expects that percentage to continue rising in the coming months as carriers belatedly attack the overcapacity burden with deeper measures other than blanked voyages.

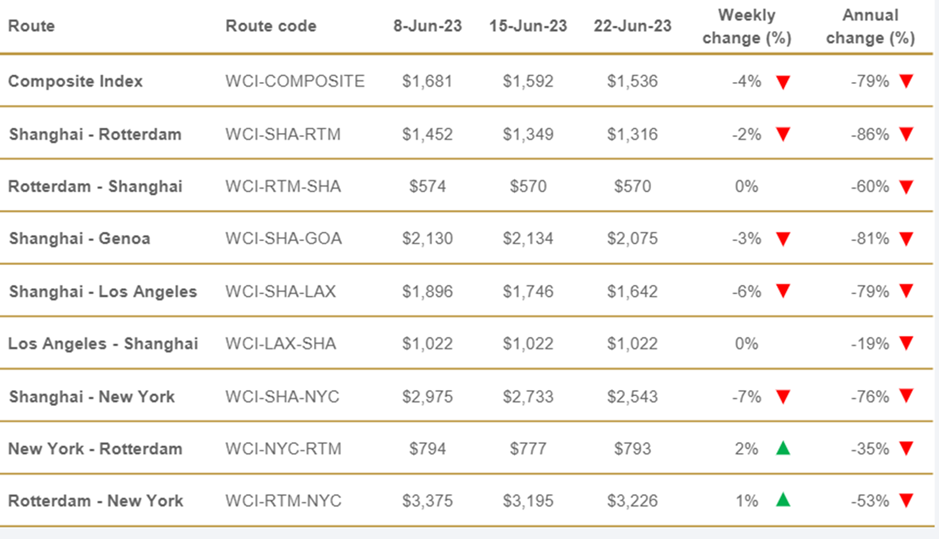

Despite carriers trying to control rate levels, the supply and demand gap is, simply put, too big to control, and rates overall continue along the downward trajectory. It is important to note that week-on-week development is minor by nature despite the clear trend.

In recent weeks' Shanghai Freight Index (spot rates), the absence of green upwards arrows is apparent and noticeable.

As we approach the traditional peak season on East-West trades, this trend is anticipated to be halted. It is not expected that carriers will be able to enforce major rate hikes, and accordingly, we assess that rate development overall will remain stable.

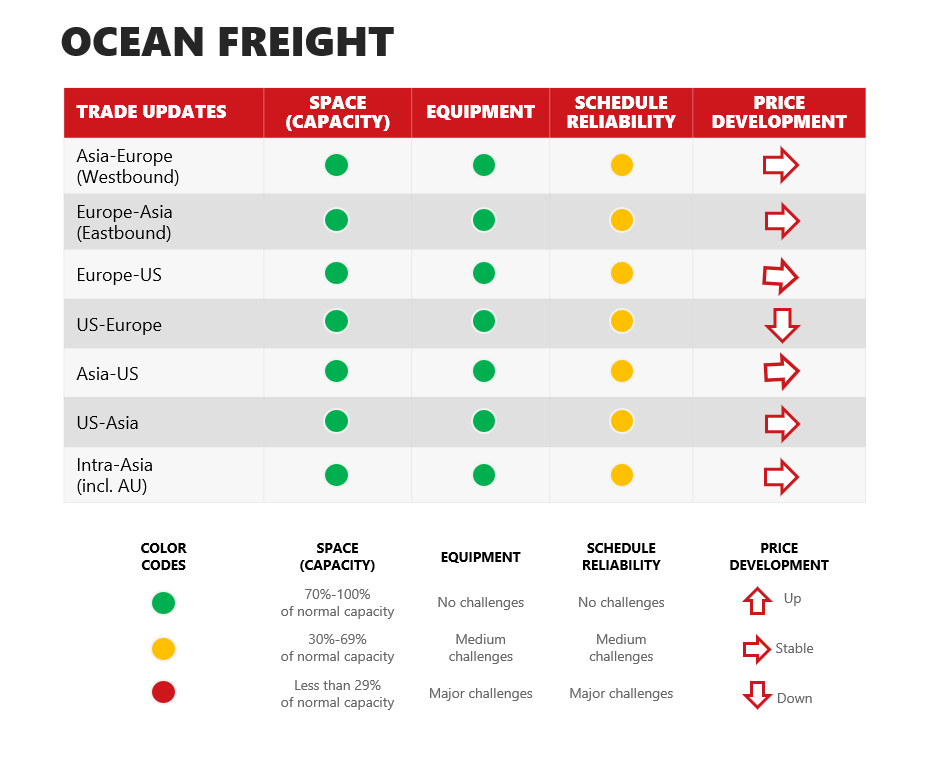

Rooted in the assessment by carriers that even an aggressive blanking program will not be sufficient to push rate levels up, current blanking programs are defensive by nature and do not pose a significant volatility threat. As seen below, scheduled blankings constitute only 3 to 5 % of the total capacity across trades.

The US West Coast strike avoided

In other news, shippers in the US can draw a sigh of relief after the PMA and ILWU reached a tentative agreement on a new labour agreement covering 29 west coast ports which comes after a full year of negotiations. Some potential disruptions can still occur until both parties officially sign the agreement.

Panama Canal restrictions postponed with rainfall providing relief

Another topic that has received significant coverage is the ongoing Panama Canal challenges. A lack of rainfall has seen water levels drop in the two artificial lakes that supply the canal with water, prompting authorities to reduce shipping traffic through the canal, which links the Atlantic and Pacific oceans.

The latest news is that the Panama Canal will postpone depth restrictions that were set to affect the largest ships crossing the key waterway. This move comes after recent much-needed rainfall that has provided some relief to the constrained maritime passage. A series of measures were scheduled to go into effect on 25 June and 9 July, requiring ships to float at higher depths, meaning they needed to carry less cargo or otherwise shed weight and impacting trade at one of the world's busiest commercial crossings.

The administration has not specified the duration of the postponement but mentioned that water levels will continue to be monitored and 'announce future draft adjustments in a timely manner'. Since the beginning of the year, the canal had instituted a number of depth restrictions as a drought caused by the El Nino weather phenomenon had put pressure on its water supplies.

Picture source: https://edition.cnn.com/2023/06/13/americas/panama-canal-water-levels-climate-intl-latam/index.html

A similar situation is causing issues in Germany, with water levels on the Rhine River falling to record levels following an extended drought period. In a similar fashion to the situation in Panama, this is preventing ships from sailing fully loaded. The challenge is causing disruption on most of the river South of Duisburg and Cologne, including the chokepoint of Kaub. Rain forecasts do provide some form of hope in the coming weeks; however, continued disruption is expected.

Outlook

Considering the challenges experienced in recent years, the current outlook shows increased reliability (currently at 70%) and a low level of disruption.

While isolated incidents like the ones just described will continue to have an impact, the general outlook is positive for shippers across industries, with carriers scratching their heads in terms of how the coming years will transpire in terms of earnings.

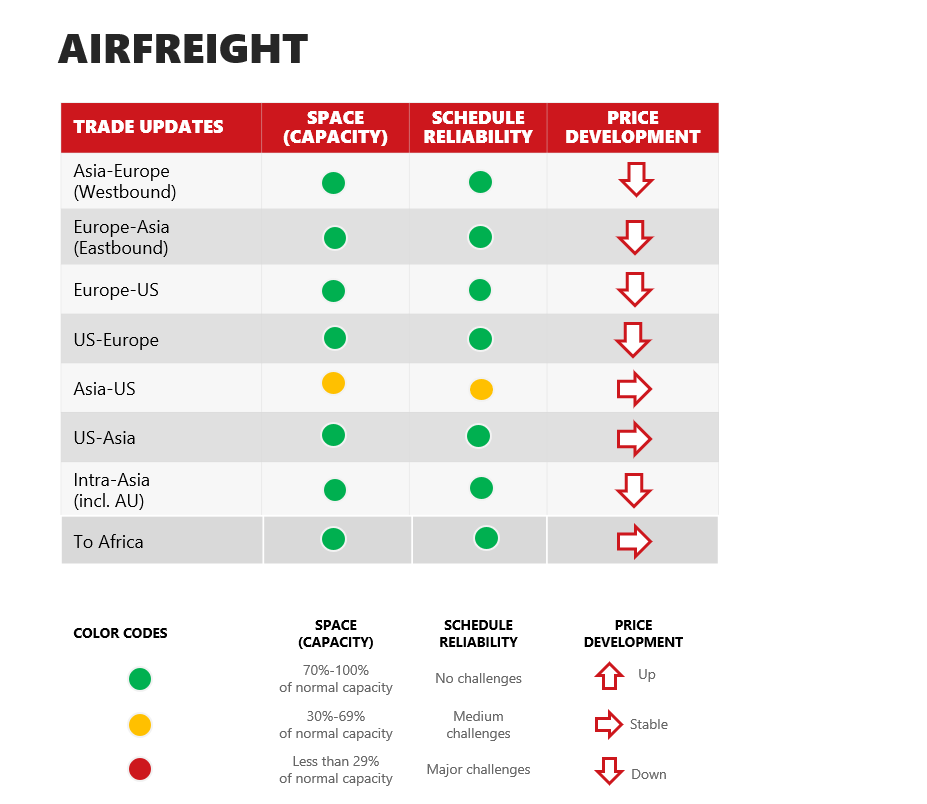

According to an article in The Loadstar published on 23 June, the air cargo market in recent week enjoyed a rare spell of sunshine, reporting a noticeable tightening of airfreight cargo capacity.

Quoting the article: 'The TAC Index noted that its overall Baltic Air Freight Index rose 1% last week, ending 'a long series of weekly declines'. WorldACD, meanwhile, reported that global tonnages were down just 4% in the first two weeks of June, a significantly smaller year-on-year gap than in previous months.'

Analysts have a growing sentiment that some major retail companies have gone too far in terms of slashing inventory levels, which in turn could force an increased last-minute rush usage of airfreight.

The opposing choir of analysts consider this a bleep on the radar with an expectation that the airfreight market will remain subdued. A factor supporting this view is the increased stability and, accordingly, predictability on the ocean freight side, making it easier to, again, plan basis ocean freight, reducing the need for urgent airfreight shipments.

Capacity continues on an upwards trajectory

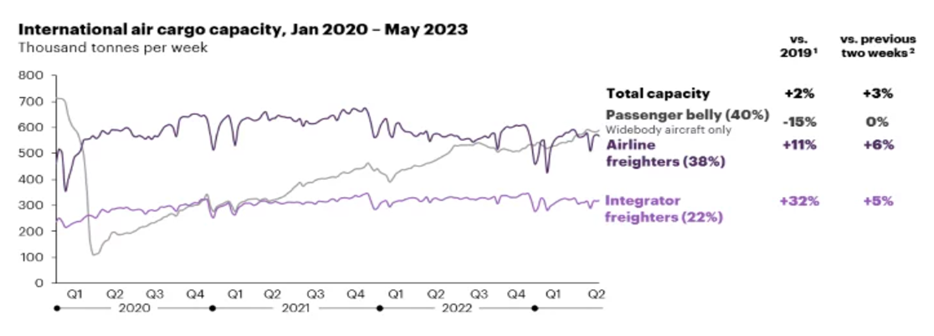

Unsurprisingly, gross available capacity continues to increase, fueled by both pure freighter capacity and increased passenger belly-hold capacity.

As seen on the graph, total capacity is up by 2 % vs pre-pandemic levels (2019), marking a full recovery on the supply side. Passenger belly-hold capacity remains the largest contributor, while freight capacity resurgence seen during recent years is still apparent at +11 % vs 2019.

Typically airlines, including cargo operators, find it difficult to control capacity levels, as seen on the ocean freight side. Some airlines have cancelled single rotations of freighter flights; however, this is not expected to have a material effect.

Outlook

We maintain a view that supply will exceed demand for the foreseeable future. Capacity supply will decrease slightly after the summer holiday period due to a decreased number of passenger flights; however, as stated earlier, not to an extent that will impact the overall supply and demand situation.

A demand increase is likely to occur only if the macro and geo-political situation changes for the better. The decreasing inflation levels will have some form of positive impact, and, as cited earlier on, some analysts predict that the over-inventory slashing has been taken too far and thus could prompt a surge in airfreight demand.

In other words, the limbo mode continues.

From a reliability perspective, service disruptions have been at a minimal level in recent weeks and months, and we expect this development to continue short and mid-term.

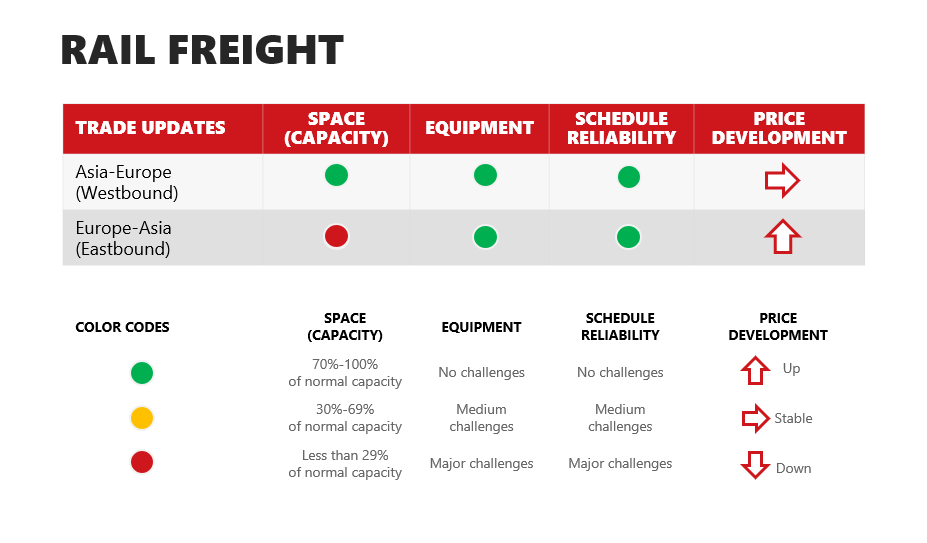

Westbound

The Xi'an rail platform will, from 1 July, launch a 2nd "Full Scheduled Train" (FST), aka 'Express Rail', departing each Saturday with a station-to-station transit time of only 14 days. Initially, there will be two weekly FST departures from China to Germany.

Conventional rail departures are naturally also available still with overall reliability considered stable.

The rail freight market generally has a close correlation to the ocean freight market, and accordingly, an apparent softening of rail volumes has been noticeable so far in 2023.

Eastbound

On the Eastbound trade, rail carriers apply a similar focus on reducing lead times with the very first 'Full Schedules Train' (FST) now introduced also with a station-to-station transit time of 14 days. Initially, the service will run from Duisburg to Xian. The first departure is on 27 June.

The central government in China has decided to suspend subsidies for the Xian Eastbound rail service, and as a result, all trains from Hamburg to Xian have been cancelled.

This has had an immediate effect on available capacity from Germany to China, i.e., to Wuhan, Chongqing, Zhengzhou, Yiwu, etc., and this tightening is expected to continue for the foreseeable future.

Want the whole advisory in PDF format? Download it here

Follow us on

Login

Login