Login

Login On behalf of Scan Global Logistics

Global Chief Commercial Officer

Market update

08 Jul, 2026

Although the Strait of Hormuz remains open to commercial traffic, we are far from a full return to normal. Vessel traffic in the strait has steadily increased since the US–Iran memorandum was agreed in June. However, negotiations on the future management of the Strait remain unresolved, and shipping continues under heightened security measures. This leaves the situation vulnerable from day to day while geopolitical negotiations continue.

New attacks from both Iran and the US cast doubts on peace agreement

Tuesday night, news broke that both Iran and the US engaged in a serious escalation of the fragile truce, with both sides accusing the other party of violating the peace agreement. “Iran’s demonstrated aggression was unwarranted, dangerous, and a clear violation of the ceasefire,” US Central Command said, referring to the three tankers, including a Qatari LNG vessel, that were struck within hours in the Strait. [1] Wednesday, US President Trump said, that the ceasefire agreement with Iran is "over", blasting the country's leadership as "scum" and "cuckoo" after fresh exchanges of fire. [2]

Iran responded by launching attacks on US military sites in Bahrain and Kuwait, with the Islamic Revolutionary Guards Corps claiming 85 facilities had been targeted. Air raid sirens were heard in both countries, and the Kuwaiti army said air defences were confronting “hostile” missile and drone attacks, but there was no confirmation of any damage.

Experts have said that the vague wording of the memorandum of understanding (MOU) has left both sides interpreting the agreement in different ways, with the repeated misunderstandings posing a continued threat to the ceasefire.

Wednesday’s attacks were the latest in a string of ceasefire violations between the two sides, despite a truce that came into effect in April, and the MOU last month that began 60 days of negotiations to resolve the issue of Iran’s nuclear program and bring a permanent end to hostilities. This development will yet again prompt uncertainty over a lasting peace agreement that includes safe and free passage through the Strait of Hormuz.

Adding to the misery, the news comes after Gemini partners Hapag-Lloyd and Maersk earlier this week announced that they will partially resume passage through the Red Sea and the Suez Canal with their SE3 service. This was long-awaited news for shippers around the world, triggering hopes of a full return to Suez Canal routing. However, safe passage now hangs in the balance with the ever-present threat of attacks by the Iran-backed Houthi rebels.

Early peak season & volume frontloading trigger ocean freight capacity chaos

Container spot rates have, during the last 8 weeks, surged to a post-pandemic high, driven by a multitude of factors.

US importers persistently try to get ahead of further tariff uncertainty, and retail inventory replenishment across most of the larger Western economies has been significantly stronger than expected. Add on top that the Red Sea diversion continues, which, in effect, causes a net capacity loss of approximately 10-15%, and you have a perfect storm cocktail.

Container carriers have moved quickly to seize the opportunity to capitalise on the spot rate freight market by introducing GRIs (General Rate Increases) as well as Peak Season Surcharges on most East-West trades. Container carriers have yet again demonstrated that they enforce stricter discipline to control supply and demand, having learned a very profitable lesson during the COVID-19 period.

Lars Jensen, a leading global container shipping analyst, points out: “The core drivers behind this sharp surge in freight rates are indeed robust demand and fully loaded vessels. The volatility experienced during the pandemic made shipping lines realise that freight rates can fluctuate entirely based on supply and demand – without being rigidly pegged to transport costs – a logic that differs in no way from that of most other industries.” [3]

All in all, the current situation, despite the impact from the closure of the Strait of Hormuz, has come as a surprise to most industry experts, yet again showcasing the volatile nature of the containerised ocean freight ecosystem.

Read on as we dive further into this topic and a range of other topics that are currently shaping the global logistics and transportation landscape.

All information is given to the best of our knowledge and cannot be considered market guidance.

Oil prices ease, but freight rates remain stubbornly high

Oil prices have eased from the highs seen during the peak of the Middle East crisis, but the transportation sector overall continues to operate in a higher-risk environment. However, after US President Trump said the ceasefire was over, the prices jump 6% to 78.63 USD a barrel, underlining the volatile situation.

The immediate risk of a major oil supply shock has though eased as exports through the Strait of Hormuz has continued to recover and OPEC+ has approved a further production increase from August. Oil prices have fallen significantly from the highs seen during the Middle East conflict, reflecting growing confidence that Gulf oil exports will continue to flow.

However, the market is far from fully normalised. Shipping activity through the Strait of Hormuz remains below historical levels, and energy flows have not yet returned to pre-conflict conditions.

While the Strait of Hormuz remains the primary focus for global energy markets, recent developments in Russia highlight that energy-related supply risks are not limited to the Middle East. Growing fuel shortages in parts of Russia following attacks by Ukraine on fuel facilities and energy infrastructure are putting additional pressure on domestic fuel availability and prices.

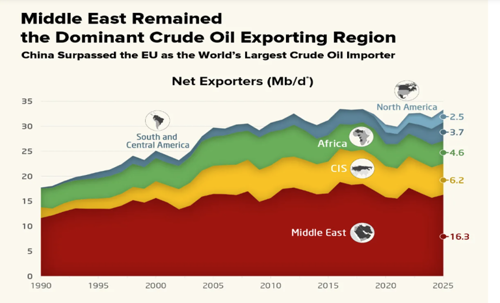

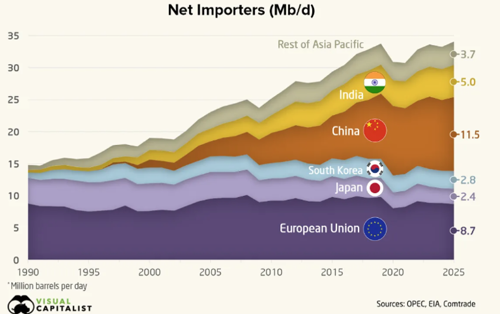

China is another important factor. As the world's largest crude oil importer, China has become a key influence on global oil markets. Recent reports suggest that weaker Chinese import demand has helped offset some of the supply disruption from the Middle East, contributing to softer oil prices.

Source: Visual Capitalist

A return to lower oil prices does not automatically translate into lower transportation costs immediately. Fuel-related surcharges introduced during the conflict are generally based on longer-term fuel procurement, risk exposure and carrier operating costs rather than daily oil price movements. While crude prices have eased over the period many transportation providers are still absorbing higher insurance costs, disrupted routing patterns and continued uncertainty around one of the world's most important energy corridors. As a result, freight pricing remains above pre-conflict levels across all transport modes.

This is another reminder that the Strait of Hormuz still carries a significant share of global oil and LNG (Liquefied Natural Gas) exports, and any renewed disruption could quickly affect fuel costs, transportation pricing and general supply chain reliability.

USMCA under review creates new uncertainty for North American supply chains

After years of nearshoring momentum, the future of North America's most important trade agreement is no longer guaranteed.

One of the most significant trade developments in recent weeks has been the Trump administration's decision not to renew the USMCA in its current form during the agreement's scheduled review process. While the treaty remains in force and does not immediately expire, the inability of the US, Canada and Mexico to reach a renewal agreement has pushed the pact into a period of annual reviews and prolonged political uncertainty.

For supply chains, the importance of USMCA extends far beyond tariffs. Over the past several years, manufacturers have increasingly adopted North American sourcing and nearshoring strategies to reduce dependence on Asia, particularly in sectors such as automotive, electronics, industrial production and consumer goods.

Although no immediate disruption is expected, any future changes to market access conditions, rules of origin requirements or tariff structures could influence manufacturing footprints, supplier strategies and freight flows across North America. The development comes at a time when many companies are already reassessing sourcing strategies due to geopolitical tensions, tariff uncertainty and ongoing efforts to build more resilient supply chains.

EU ends de Minimis exemption for low-value imports

A significant change to European customs rules took effect on 1 July 2026, as the EU removed the long-standing customs duty exemption for goods valued at EUR 150 or less. Low-value parcels entering the EU from non-EU countries are now subject to a temporary EUR 3 customs duty, ending a system that for years allowed billions of e-commerce shipments to enter duty-free.

The move is part of the EU's broader customs reform programme and is designed to address the rapid growth in direct-to-consumer imports, particularly from major online marketplaces such as Temu, Shein and AliExpress. According to the European Commission, nearly 5.9 billion low-value items entered the EU in 2025, creating mounting pressure on customs authorities and concerns about product safety, regulatory compliance and fair competition for European businesses.

Industry experts expect it to reshape e-commerce supply chains, as online marketplaces are already adapting by increasing the use of European fulfillment centres and shifting goods into the EU in bulk rather than shipping individual parcels directly to consumers. Similar changes were observed after the US removed its own de minimis exemption, leading to a decline in direct parcel volumes and an increase in the use of regional warehousing and distribution networks.

In much-awaited news, Hapag-Lloyd and Maersk on Monday, 6th July, announced that their SE3 service from Asia to Europe, with immediate effect, would utilise passage through the Red Sea and Suez Canal.

This move underlines the cautious approach to resuming passage through the Red Sea and the Suez Canal. It is considered that a full return to the preferred routing via the Red Sea and Suez Canal is not a matter of weeks, but rather months, and with a fresh escalation in the Iran-US war, new safety doubts have emerged.

Looking ahead, a gradual increase in Suez Canal utilisation continues to appear more likely than an abrupt reopening. While shorter transit times would improve service efficiency, carriers are also aware that a sudden large-scale return could release significant vessel capacity into an oversupplied market, placing downward pressure on freight rates.

Summer freight rate surge catches the market off guard

Ocean freight rates have surged across nearly every major trade lane for 10 consecutive weeks. However, first cooling-off indications have emerged with the latest SCFI data splitting the market in two: The Transpacific trade is still charging higher, while the Asia–Europe trade reports only moderate increases and Asia–South America backs off from its recent peak.

Despite the first signs that rates have reached a form of plateau level from Asia to Europe, the increases over the period are severe and remarkable. On the Asia-Europe trade rate levels are up by more than 60% vs. 2025 - Asia-US West Coast rate increases have passed the 200% mark, and East Coast is clocking in at an increase of 101%.

The traditionally volatile trade from Asia-South America has been in a league of its own. After topping out at $16.424/40' in late June, rates fell back this week to $14.460/40'. Yet the lane is still more than double its April level and sits among the highest-priced in the market.

See the latest SCFI developments below, illustrating week-on-week, last 4 weeks and year-on-year rate changes.

While SCFI reflects short-term rate developments, a similar pattern is evident in long-term contracted rates. Carriers across the board have implemented hefty Peak Season Surcharges on both the Asia-Europe and Transpacific trades, with the latter leading the way. Additionally, container carriers have in many cases cut and reduced weekly allocations, putting further pressure on shippers.

This development once again makes it very clear that when the gap between short- and long-term rates becomes too big, carriers will act to capitalise on the situation, even if it means adjusting long-term agreed rates.

We recommend proactive, early planning for especially high-priority shipments and encourage ongoing dialogue with your assigned SGL contact person.

Port bottlenecks intensify congestion risk across major hubs

Global port congestion has intensified significantly during June, reaching its highest level since 2022. According to market intelligence provider Linerlytica, 10.9% of the global container fleet is currently tied up in port queues and anchorages, effectively removing capacity from the market and contributing to tighter supply conditions [4].

North Europe remains one of the most affected regions, with continued congestion in Rotterdam, Antwerp, Hamburg and other key gateways. Recent communication from Maersk highlights that a June heatwave caused temporary terminal stoppages and productivity losses in Rotterdam, reducing handling efficiency and creating short-term schedule disruptions [5].

In Antwerp, pilot shortages continue to affect vessel movements, while elevated yard pressure remains an issue across the region. Customers are being advised to build additional buffer time into their supply chain planning and accelerate import pick-ups to ease terminal congestion.

In parallel, Mediterranean ports are entering the traditional summer pressure period, with Genoa expected to experience seasonal productivity challenges.

US ports are overall operating under normal conditions, though we experience slight disruptions in the East Coast ports with berth waiting times of 1 day. If your cargo is bound for inland destinations via rail, you should expect average dwell times of 5-8 days on the West Coast, while on the East Coast, the rail dwell time is 2-4 days.

Zooming in on Latin America's main ports in Brazil (Santos and Paranaguá), Chile (Valparaíso), and Colombia (Cartagena), these ports operate with normal berth waiting times, and overall, we do not currently experience major operational challenges in these ports.

In the Middle East, several ports remain affected by the schedule reshuffling that carriers had to implement due to the situation in and around the Strait of Hormuz.

Initially, carriers were forced to discharge containers bound for the Persian Gulf at alternative ports, causing the first “shock” effect at those ports. Later, as carriers started to offer “land bridge” solutions to the Gulf States via Jeddah, King Abdullah, Salalah, Sohar and Fujairah, the congestion level in the affected ports increased significantly and is still affected by the sudden increase in volumes routed via these ports.

Finally, the demand surge on the Far East Westbound and Transpacific trades has had a noticeable and instant impact on congestion levels in Asia, with the world’s busiest port, Shanghai, as well as the main hubs in Ningbo and Qingdao, reporting waiting times of up to 4 days. The major transit hubs in South-East Asia, i.e. Singapore, Tanjung Pelepas and Port Klang, are only modestly disrupted with expected berth waiting times of up to 1.5 days.

May records best global schedule reliability performance of 2026

Over the past 12 months, global schedule reliability has been stable in the range of 62-65%. The latest Global Liner Performance report, published by Sea-Intelligence on June 29, reports month-on-month improvements across all major trade-lanes except from the backhaul trade from Europe to Asia, which had a -1.7% decline.

Year-on-year global schedule reliability dropped slightly from 65.9% to 64.7%, however, looking at 2026, the development is positive, with May recording the best performance year-to-date.

While the Gemini Alliance, i.e. Hapag-Lloyd and Maersk, has consistently performed above 70% during 2026. MSC managed to improve its on-time reliability and has now reached 71.6% on this important KPI for carriers and, not least, their customers. CMA CGM came in just short of the 70% mark at 69.9%, while the rest of the pack is trailing behind at around 60%.

Airfreight enters July with tight capacity and rates holding firm

The global airfreight market enters July with a strong demand, however, also with a full capacity rebound. Rotate’s June report shows a 4% capacity growth, as capacity declines to and from the Middle East was largely offset by direct Asia-Europe capacity.

The sustained demand, in turn, continues to fuel yield levels that are now up by 44% vs 2025 levels, with this development being aided by increases in fuel costs of up to 38%.

Capacity utilisation on key corridors is now close to its practical maximum. Asia-North America is operating at a dynamic load factor of 90%, while Asia-Europe and Asia-Middle East both stand at 87%. In a normal market, 90% is close to the practical ceiling for air cargo, as not every flight on these routes is configured or positioned to maximise cargo uplift. In practical terms, these corridors are effectively full, and the pressure is driven by more than just disruptions in the Middle East.

Major injection of capacity only expected as of 2028 and onwards

All airlines continue to be plagued by persistent delays in new aircraft deliveries. The demand is there: during the first quarter of 2026, commercial aircraft manufacturers received nearly 570 orders for new aircraft, making it the strongest first quarter for orders since 2013.

Deliveries, however, told a different story. Manufacturers handed over 261 aircraft during the same period, around 4% fewer than in the first quarter of 2025. According to IATA, the global aircraft backlog has now grown to more than 18,000 aircraft. [6]

The delays are triggered by factors such as delays in engine manufacturing; however, supply chain constraints remain the industry's biggest challenge, particularly those linked to labour shortages that continue to affect manufacturers across multiple tiers of production.

Due to a collapse in demand during the COVID-19 pandemic, manufacturers and suppliers reduced their workforce and scaled back production. However, air travel recovered much faster than many had anticipated, leaving companies scrambling to rebuild capacity and meet renewed demand for aircraft.

Presently, there is no immediate relief in sight, and the current outlook is that aircraft deliveries will dip in 2028 and only then rebound, as illustrated below, courtesy of Rotate.

Rates stay high despite Gulf capacity returning

In week 25, average global air cargo rates edged up 1% to USD 3.24 per kg, leaving worldwide rates 35% higher than the same period last year. Spot rates also increased by 1% to USD 3.75 per kg, standing 47% above last year’s level.

Although capacity is returning to Gulf markets, rate relief is not keeping pace. On the MESA-Europe corridor, capacity increased by around 13% in week 25, well ahead of the 2% rise in chargeable weight. Despite this, average spot rates remained almost unchanged at USD 3.76 per kg, down just 1% week on week.

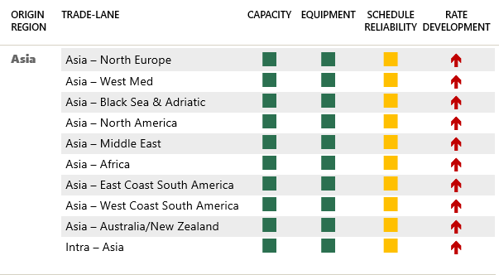

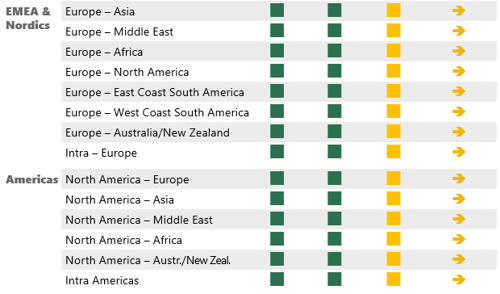

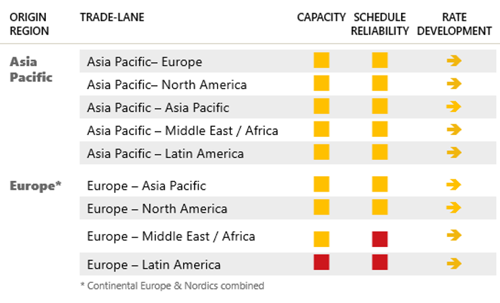

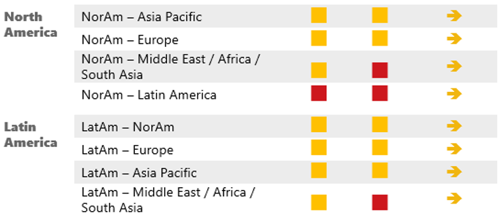

TRADE LANE OVERVIEW OF OCEAN FREIGHT

TRADE-LANE OVERVIEW OF AIRFREIGHT

Global Chief Commercial Officer