Login

Login Get in touch

Mads Drejer

Global Chief Commercial Officer

Email me

Market update

20 May, 2026

A coalition of over 40 nations stated they are committed to the Multinational Military Mission (MMA), led by France and the UK, to reopen the Strait of Hormuz once a ceasefire has been agreed.

Those involved in the international project have disclosed plans to deploy a wide variety of high-end aviation and naval equipment to safeguard the troubled waterway – an effort that could revive global trade, long strained by Iran’s blockade.

Peace talks in a continued deadlock

US President Trump announced on Monday, 18 May, that he was calling off what he said was a scheduled attack on Iran that was supposed to happen the following Tuesday. The US president said he made the decision because "serious negotiations" were taking place toward a peace deal that would be acceptable to the US and countries in the Middle East.

It is also clear that Iran shows no sign of budging despite a crippled economy and growing internal unrest. The latest proposal from Iran includes “the country’s insistence on its right to uranium enrichment and peaceful nuclear activities.” Additionally, demands included an end to the conflict on all fronts, including Lebanon, the lifting of the US naval blockade, lifting of “all unilateral sanctions, release of frozen Iranian funds and war damage compensation”. The demands led the US to issue an instant rejection, with President Trump calling them “totally unacceptable” and a “piece of garbage”. [1]

As we speak, it could be days, weeks or months, and it is anyone’s guess where the peace talks will end or whether a new armed conflict will be the result.

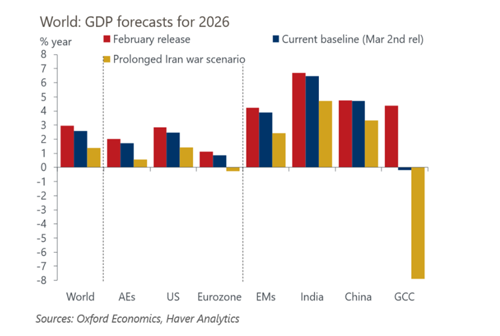

Leading global economies in a state of paralysis

Valdis Dombrovskis, European Commissioner for Economy and Productivity, told CNBC that the spring forecast, to be released later this week, will see economic growth figures adjusted downward and inflation figures adjusted upward. “We are facing a stagflationary shock,” he said on Monday, 18 May, on the sidelines of the meeting of G7 finance ministers in Paris. [2] Fears of stagflation have risen in recent weeks, with a lasting settlement to the war in the Middle East proving elusive, and with the vital Strait of Hormuz closed, oil prices remain above $100 a barrel.

So, what is stagflation in reality? It is, in essence, a perfect storm defined by the simultaneous occurrence of three factors being high inflation, slow economic growth and lastly high unemployment rates.

Stagflation is, amongst financial experts, considered the “worst of all worlds”. To put it further into perspective, Europe last experienced a severe period of stagflation in the 1970s, triggered by the 1973 Arab oil embargo and the 1979 Iranian Revolution. These supply-side energy shocks quadrupled oil prices, leaving European nations with soaring inflation rates, high unemployment, and stagnant economic growth.

A “prolonged war” scenario issued by Oxford Economics outlines the serious situation, projecting a potential negative growth for Eurozone countries if the situation does not change.

Source: Oxford Economics

For global supply chains, the conclusion is clear: this is not only a regional maritime disruption. It is a broader cost and growth storm that will impact supply and demand across all transport modes.

Oil price roller-coaster ride

Oil prices have settled firmly above $100 per barrel, amidst mixed signals from US President Donald Trump on whether he will resume military strikes against Iran or continue peace talks. Goldman Sachs forecasts that every month the Strait of Hormuz remains closed and adds $10 to the price of oil by end of year, said Daan Struyven, Head of Oil Research at the investment bank. [3]

The oil market has been reacting swiftly to any signs of progress, or lack of it, towards a peace deal that will reopen the Strait of Hormuz. Day-to-day volatility aside, the picture is clear and offers no sign of relief for the global economy.

Source: Trading Economics

How real is the threat of a potential oil shortage?

With a wide range of airlines having announced cancelled passenger flights to weather the worst of the oil supply and cost shock, speculation is rapidly increasing about whether we could at some point face an actual fuel shortage on a broader scale.

In an interview with The Loadstar, Cargolux CEO Richard Forson shared insights into the current situation by stating that “consequences of the Iran conflict could extend far beyond aviation and warned that jet fuel shortages would be the least of our worries if the crisis continues for several months.”

He added: “For me, if the Middle East situation continues, I think at some point there will be a shortage. Governments around the world do have emergency stocks on hand, but those are not meant to cover month after month of shortages.”

He did, though, double down on his comments that jet fuel is the least of our worries by saying: “One thing that is built into every single product that we consume is logistics. With the price of energy needed for logistics increasing significantly, this is obviously going to be passed on to the consumer.” [4]

It is generally considered that we are not at risk of seeing severe fuel shortages in the short and mid-term. It is more the cost pressure that poses a threat, as evidenced by Spirit Airlines in the US, which entered liquidation at the beginning of May, crushed by compounding debt and a massive fuel-price shock.

Ocean freight disruption persists

The temporary US-Iran ceasefire announced in early April has not translated into a normal operating environment for commercial shipping. Vessel transits through the Strait of Hormuz remain limited, carriers and insurers continue to treat the area as high risk, and Iran has moved towards tighter control of passage through the strait.

There are signs of limited movement, but total transit levels remain more than 90% below normal. In practical terms, Hormuz may be politically described as open in selected cases, but it is not functioning as a predictable commercial corridor.

Maritime risk has also spread beyond the strait itself. Recent incidents include:

A vessel anchored near Fujairah was seized and diverted towards Iran.

An Indian-flagged cargo vessel sank off Oman after an attack sparked a fire on board.

Iran seized the tanker Ocean Koi in the Gulf of Oman.

These incidents underline that the threat picture now extends across the wider Gulf of Oman and UAE anchorage areas, not only the narrow Hormuz Strait passage.

Ocean rate development

Rate level development is overall mixed across major trade lanes; however, with a clear upwards trajectory during the last weeks. SCFI rates from Asia to North Europe have, over the last 4 weeks, increased 21 %, settling in at USD 3.632/40´, with the corresponding number for China-Europe Mediterranean being 30 %, equivalent to USD 6.290/40´.

A similar pattern is clear on China to US routes, with East and West coast rates increasing 18 % and 21 % respectively over the period.

Rates from China to Latin America have also increased sharply in recent weeks, clocking in at 67 % increase over the last 4 weeks, passing the USD 8.000/40´ mark.

The development is primarily driven by the full effects of rising bunker fuel costs, while at the same time vessel supply remains tight. Alphaliner data shows idle containership capacity at just 0.7%, meaning the global fleet is effectively fully deployed. While demand may look stable on some trades, available vessel supply is still being absorbed by diversions, delays and ships taking shelter due to the conflict.

Airfreight hit by fuel prices

The Middle East airfreight market has improved from the immediate shock, but it has not returned to normal. Capacity is coming back in stages, especially through Gulf carriers, but Gulf capacity remains well below pre-war levels. Some carriers are still avoiding key Middle East stops, while fuel supply and jet fuel pricing are dominating the market.

Europe’s jet fuel imports from the Middle East dropped from 330,000 barrels per day in March to just 60,000 barrels per day in April. The IEA (International Energy Agency) said Europe needs to replace at least 80% to 90% of the lost Middle East volumes to avoid summer shortages, but April imports reached only 70% of March levels. [5]

Airfreight rate development

Airfreight markets have started to stabilise since the early-April ceasefire, but the recovery remains uneven. WorldACD’s latest weekly data shows that global airfreight tonnage rebounded by 5% year-on-year in April, while global average rates increased to USD 3.17 per kg, up 28% year-on-year.

The Middle East and South Asia region is also recovering, but from a heavily disrupted base. In week 18, Middle East and South Asia outbound airfreight volumes rose 2% week-on-week and was 4% higher year-on-year. For April overall, chargeable weight from the region was up 7% year-on-year, while inbound Gulf volumes improved significantly, from 40% down in March to 7% down in April.

However, capacity remains the key watchpoint. WorldACD reported that by week 17, MESA capacity was still 26% below pre-war levels, while Gulf capacity remained 46% below pre-war levels. This means airfreight is available, but the market remains exposed to sudden capacity shortages, fuel price movements and routing disruption.

As usual, we encourage you to have a close dialogue with your designated SGL contact person, both in terms of planning, as well for latest information on fuel and war risk surcharges.

We have added some alternative solutions and routings below, allowing you to have a full overview of available alternatives.